Bankruptcy Effect On Credit Score: Points Lost, Timeline

Filing for bankruptcy can stop wage garnishments, end creditor harassment, and give you a real path out of debt, but most people want to know what it costs them on the other side. The bankruptcy effect on credit score is one of the biggest concerns we hear from clients at Mayfield Law Firm, P.A., and it's a fair question. A bankruptcy filing will lower your score, sometimes significantly, and it stays on your credit report for years . But the full picture is more nuanced than the headline number suggests.

Your credit score before filing, the chapter you file under, and how you handle your finances afterward all shape the actual impact. Some filers see a drop of 100 points or less because their score was already damaged by missed payments and collections. Others with higher scores going in may lose 200 points or more. Either way, the hit is temporary , and for many people, bankruptcy creates the conditions to rebuild faster than continuing to struggle with unmanageable debt.

This article breaks down exactly how many points you can expect to lose, how long bankruptcy stays on your record, and what the timeline for credit recovery actually looks like. At our offices in Southaven, Mississippi, and Memphis, Tennessee, we've guided clients through Chapter 7 and Chapter 13 filings for over 40 years, and we've watched many of them come out the other side with stronger financial footing than they had before.

Why bankruptcy can drop your score fast

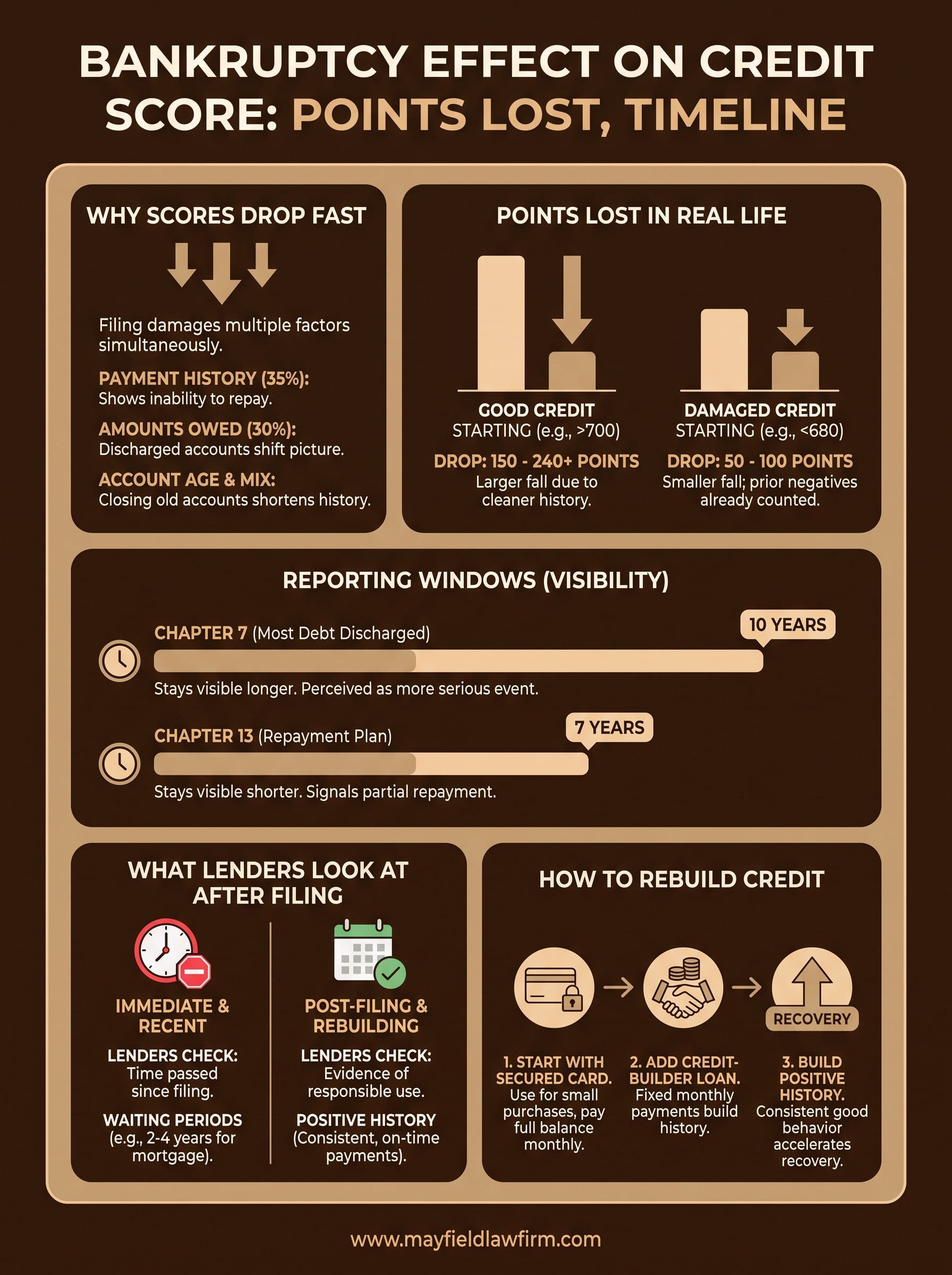

When you file for bankruptcy, credit scoring models treat the filing as one of the most serious negative events they can register. The bankruptcy effect on credit score happens quickly because the filing damages multiple scoring factors at the same time rather than just one. Understanding which factors absorb the hit explains why the drop can feel both immediate and steep.

How credit scoring models weigh a filing

FICO scores , which most lenders use, assign 35% of your total score to payment history and 30% to amounts owed. A bankruptcy filing signals that you could not repay debts as agreed, which damages payment history directly. Discharged accounts also shift your amounts owed picture and can affect your credit utilization ratio, especially if lenders close credit lines around the time you file.

Beyond those two major categories, account age and credit mix take hits when accounts close through the bankruptcy process. Losing older accounts shortens your average account age, which costs you additional points. Most people are surprised to find the score drop coming from several directions at once rather than a single entry on their report.

A bankruptcy filing affects your score on multiple fronts simultaneously, which is why the total point drop often exceeds what any single missed payment or collection would cause on its own.

Why a higher starting score takes a bigger hit

If your score was already low before you filed, the additional drop from the bankruptcy filing tends to be smaller because prior negative marks were already pulling the number down. Filers who enter with scores above 700 have more to lose and cleaner histories, so the bankruptcy stands out as the defining derogatory event and scoring models respond with a steeper drop.

Prior delinquencies also shape how much the filing moves your final score . Accounts that went past due months before you filed may have already pulled your number down, meaning the bankruptcy itself adds less incremental damage than worst-case scenarios suggest. The filing still appears as a public record and remains visible to every lender who pulls your report.

What point drop you might see in real life

The bankruptcy effect on credit score varies based on where your score stands when you file. FICO research shows that filers with scores around 680 typically lose 130 to 150 points, while those carrying scores near 780 can lose 200 points or more. These numbers give you a realistic baseline, though your personal outcome depends on your specific credit profile and the chapter you file under.

Starting with good credit

If your score sits above 700 when you file, you have further to fall. A Chapter 7 discharge on a clean credit history registers as one of the most damaging events a scoring model can record, so drops in the range of 150 to 240 points are common for filers in this group. Chapter 13 filers in the same score range often see slightly smaller drops because the repayment structure signals partial repayment of debts.

The higher your score going in, the more room there is to drop, but recovery from a stronger starting position often moves faster once the filing stops new negative activity from accumulating.

Starting with damaged credit

If missed payments, collections, and charge-offs have already pulled your score into the 500s or low 600s , the filing adds less incremental damage. Many filers in this range see drops of 50 to 100 points because prior delinquencies were already factoring heavily into their score. For some clients, the automatic stay stops new damage from piling on immediately.

How long bankruptcy stays on your credit report

The bankruptcy effect on credit score doesn't end with the initial drop. The filing stays visible on your credit report for years, and every lender who pulls your report during that window can see it. The good news is that the impact on your score weakens over time, even before the filing disappears entirely.

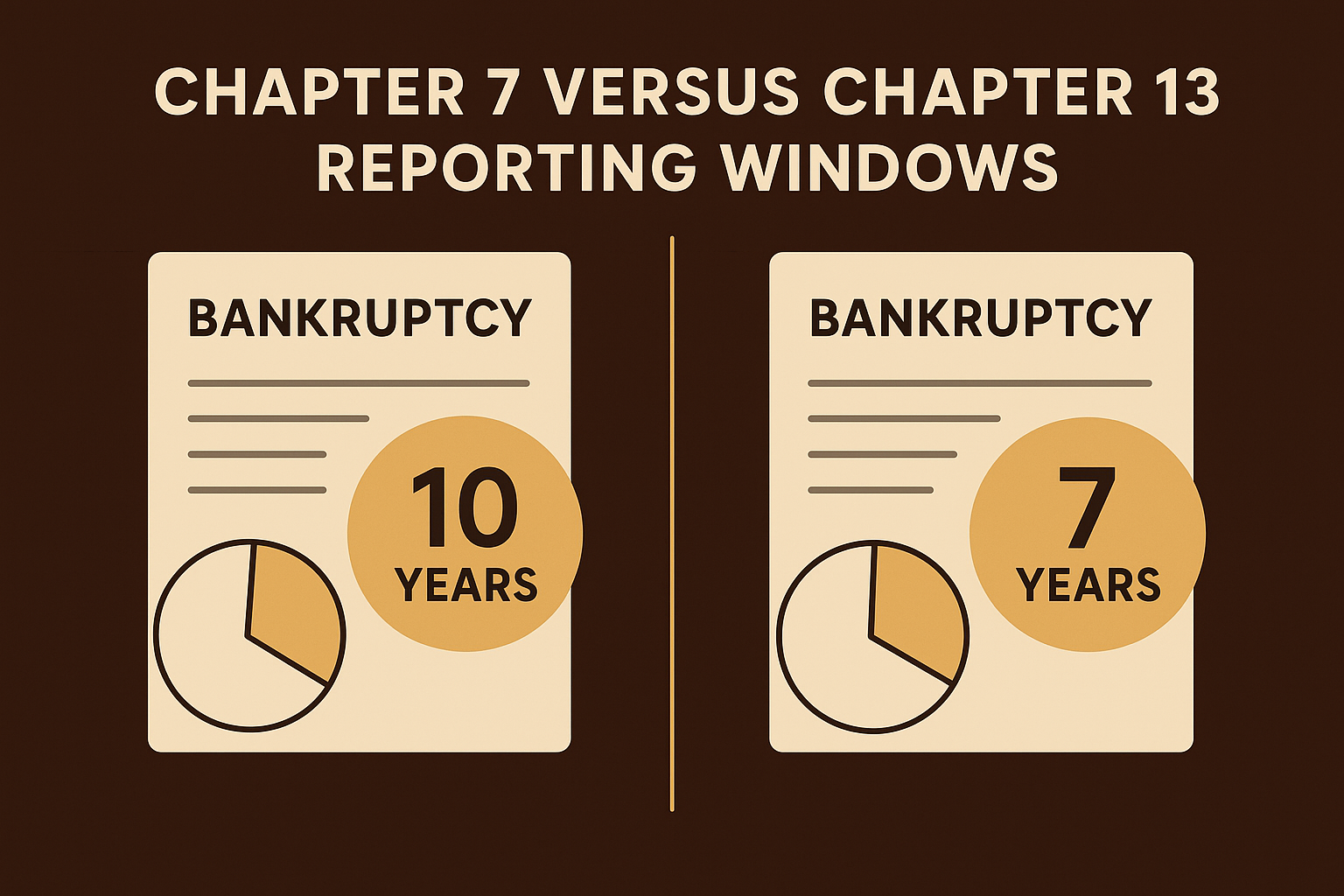

Chapter 7 versus Chapter 13 reporting windows

Chapter 7 bankruptcies remain on your credit report for 10 years from the filing date. That longer window reflects the fact that Chapter 7 discharges most debts without a repayment plan, so credit bureaus treat it as a more serious credit event. Chapter 13, which requires a three-to-five-year repayment plan before discharge, carries a seven-year reporting period from the filing date.

Choosing Chapter 13 over Chapter 7 can shorten the time the bankruptcy stays visible on your report by three years, which matters if rebuilding credit quickly is a priority for you.

How the filing affects your score over time

Your score typically improves each year the bankruptcy ages, even while it still appears on your report. Lenders also apply less weight to older negative entries, so a five-year-old filing hurts you far less than a recent one does. Building positive credit history during that window accelerates your recovery and gives newer, cleaner data more influence over your overall score.

What lenders look at after you file

After a bankruptcy filing, the bankruptcy effect on credit score is only part of what lenders evaluate when you apply for new credit. Most lenders look beyond your score and pull your full credit report to assess how you've managed money since the filing date. The bankruptcy entry itself tells one story, but the activity after it tells another.

The gap between filing and application

Lenders pay close attention to how much time has passed since your filing date. A bankruptcy filed two years ago with a clean record since then looks meaningfully different from one filed six months ago. Many conventional mortgage lenders require a waiting period of two to four years after a Chapter 7 discharge before they'll approve a loan application, and FHA loans typically require two years.

What they want to see on your report

Beyond the waiting period, lenders look for evidence of responsible credit use after the filing. Consistent on-time payments on a secured card or small installment loan signal that your financial habits have shifted. Lenders also check for new derogatory marks like late payments or collections that appeared after your filing date, since those suggest the bankruptcy didn't change your payment behavior.

Showing two or more years of clean payment history after filing can outweigh the presence of the bankruptcy entry itself in many lenders' approval decisions.

How to rebuild credit after bankruptcy

The bankruptcy effect on credit score doesn't freeze you in place permanently. You can start rebuilding within months of your discharge by taking deliberate, consistent steps that create positive data on your report and give lenders a reason to extend credit again.

Start with a secured credit card

A secured credit card requires a cash deposit that becomes your credit limit, which makes approval straightforward even with a recent bankruptcy on your report. Use it for small, predictable purchases like gas or groceries, and pay the full balance every month so no interest accrues and your payment history stays clean.

Most major banks and credit unions offer secured cards designed for people rebuilding after financial hardship. After 12 to 18 months of responsible use, many issuers will upgrade you to an unsecured card and return your deposit, which also adds account longevity to your report.

Paying your secured card on time every month is one of the fastest ways to add positive payment history to a report that a bankruptcy filing has damaged.

Add an installment loan to your credit mix

A credit-builder loan from a credit union works alongside your secured card to diversify your credit mix, which FICO scores reward. You make fixed monthly payments, and the lender reports each payment to the credit bureaus, building your history steadily over time.

Combining an installment loan with a secured card gives scoring models two types of positive accounts to weigh, which accelerates your score recovery more than using either product alone.

Next steps

The bankruptcy effect on credit score is real, but it's also manageable when you understand what's happening and why. Your score drops because multiple credit factors take a hit at once, and the filing stays on your report for seven to ten years depending on the chapter you file under. The recovery timeline moves faster than most people expect when you start building positive history immediately after discharge through secured cards, credit-builder loans, and consistent on-time payments.

Before you decide whether bankruptcy is the right move, speaking with an experienced attorney gives you a clearer picture of what your specific situation looks like. At Mayfield Law Firm, P.A., we've helped clients across Southaven, Mississippi, and Memphis, Tennessee, navigate Chapter 7 and Chapter 13 filings for over 40 years. If you're weighing your options and want straightforward answers, contact our bankruptcy attorneys for a free consultation today.