Bankruptcy Timeline: How Long Does Bankruptcy Take?

Filing for bankruptcy is a major financial decision, and one of the first questions people ask is how long does bankruptcy take from start to finish. The answer depends almost entirely on which chapter you file. A Chapter 7 case can wrap up in as few as four to six months , while a Chapter 13 repayment plan stretches across three to five years.

Understanding these timelines matters because they affect your budget, your credit, and how quickly you can move forward. Each chapter follows its own sequence of steps, from the initial filing and creditor meetings to the final discharge of your debts . Knowing what to expect at each stage helps you plan realistically and avoid surprises along the way.

At Mayfield Law Firm, P.A., we've guided clients across Northeast Mississippi and South Memphis through both Chapter 7 and Chapter 13 filings for over 40 years. Below, we break down the full bankruptcy timeline step by step, explain what factors can speed things up or slow them down, and help you figure out which path fits your situation .

Why bankruptcy timelines vary

No two bankruptcy cases move at exactly the same pace. How long does bankruptcy take in your situation depends on a combination of factors: the chapter you file under, the complexity of your finances , and decisions made by the bankruptcy trustee and the court. Getting a clear answer requires looking at each of these variables separately, because a change in any one of them can shift your timeline by weeks or even years.

The chapter you file is the biggest factor

The single largest driver of your timeline is whether you file Chapter 7 or Chapter 13 . Chapter 7 is a liquidation bankruptcy where a trustee reviews your assets, wipes out eligible unsecured debts, and the court issues a discharge in roughly four to six months . Chapter 13 requires you to propose and complete a three-to-five-year repayment plan before the court discharges your remaining eligible debts. The difference in duration isn't a design flaw; it reflects the distinct purpose each chapter serves.

Chapter 7 works best for people with limited income and few non-exempt assets, while Chapter 13 suits those with regular income who want to catch up on secured debts or protect property they would otherwise lose in liquidation.

Your financial picture adds complexity

The more complicated your assets, income sources, and debt types , the more documentation you need to gather and the more the trustee needs to review. If you own rental property, run a sole proprietorship, or carry a mix of secured loans and credit card debt, the trustee will likely ask additional questions and request more supporting records. Your credit history, the number of creditors listed, and whether any creditors are likely to challenge your filing all factor into how smoothly the case progresses. Cases with straightforward W-2 income and standard consumer debts tend to move faster because there is simply less for everyone to sort through. Incomplete or inaccurate paperwork at the time of filing is one of the most common reasons timelines stretch longer than expected.

Court schedules and trustee actions set the calendar

Even a well-prepared case moves at the court's pace. Your 341 meeting of creditors (the required hearing where the trustee asks you questions under oath about your finances) must be formally scheduled, which typically adds several weeks after your filing date. If a creditor objects to the discharge of a specific debt or the trustee finds a discrepancy in your paperwork, the court must resolve those issues before moving forward. Submitting all required documents on time and completing your mandatory credit counseling before filing are two of the most practical steps you can take to avoid unnecessary delays.

How to estimate your bankruptcy timeline

You can build a rough estimate before you speak to an attorney by examining two key factors : the chapter you are likely to qualify for and the processing pace of your local bankruptcy court . Both pieces of information are accessible before you file a single document, and together they give you a working baseline you can refine as your situation becomes clearer. Pinning these down early prevents the frustration of planning your finances around a timeline that turns out to be weeks or months off.

Start with the means test

The Chapter 7 means test compares your household income to the median income for your state and family size. If your income falls below that threshold, you likely qualify for Chapter 7. If it exceeds the median or you have significant disposable income after allowed expenses, Chapter 13 is the more probable path . Each outcome points to a very different commitment:

- Chapter 7: Four to six months from filing to discharge

- Chapter 13: Three to five years through a structured repayment plan

Answering the means test question first is the most direct way to get a realistic sense of how long does bankruptcy take in your specific situation.

Account for your local court's schedule

Court processing times vary by district, and those differences directly affect your personal timeline. Your 341 meeting of creditors is typically scheduled three to five weeks after your filing date , and creditors then have 60 days from that meeting to raise formal objections before the court can move toward discharge.

Your attorney can pull current processing data for your district and factor it into a realistic estimate. Courts in the Northern District of Mississippi and the Western District of Tennessee each run on their own calendar, so local knowledge matters when you are trying to set a dependable end date.

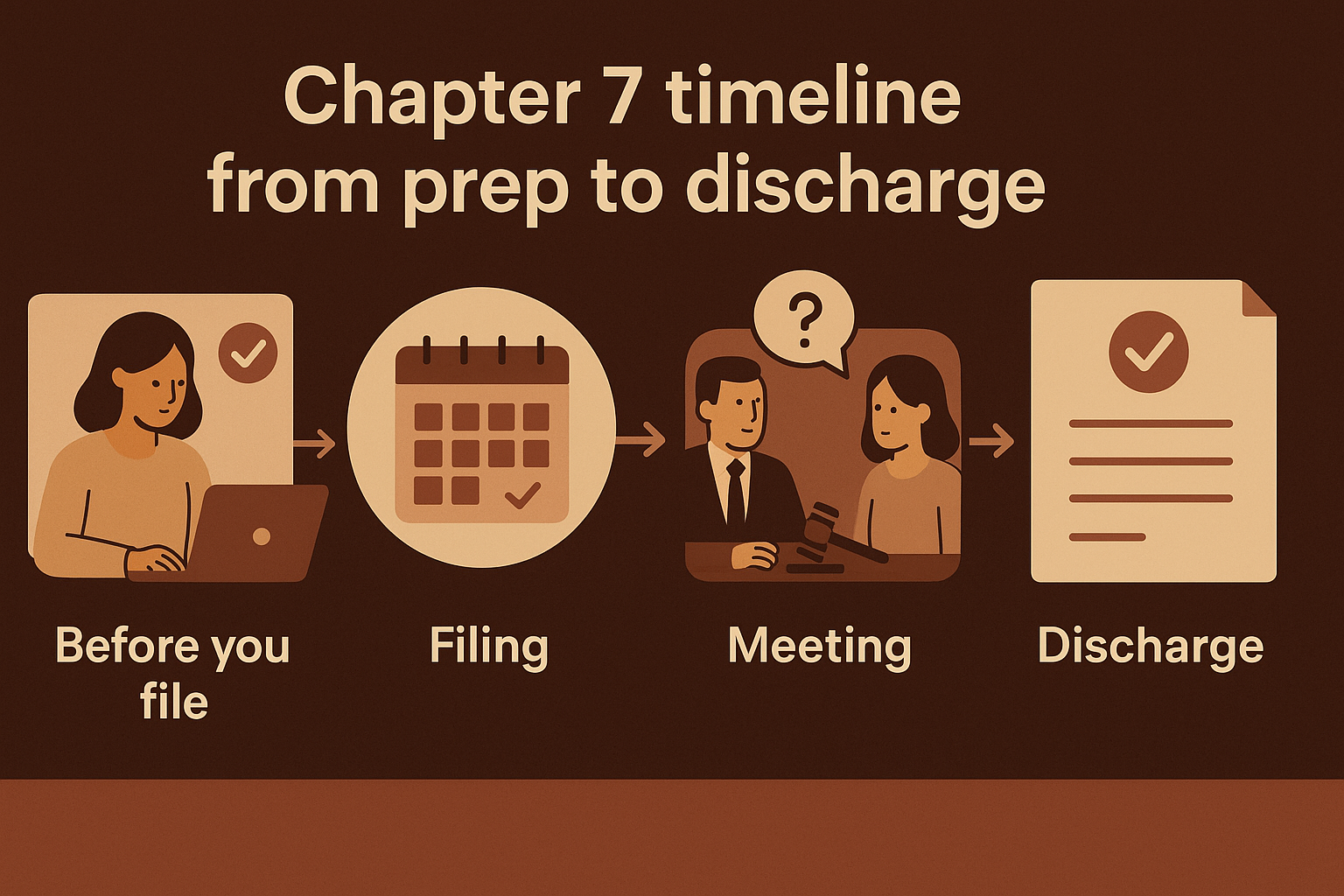

Chapter 7 timeline from prep to discharge

Chapter 7 is the fastest path through bankruptcy , and if you're wondering how long does bankruptcy take under this chapter, the short answer is four to six months from your filing date to discharge. Most of that time is spent waiting on the court's scheduling calendar rather than doing active work, which means your preparation before filing directly determines how smoothly the case moves.

Before you file

Before your case number is assigned, you must complete a credit counseling course from an approved provider , which takes roughly one to two hours. You'll also need to gather financial records including recent tax returns, pay stubs, bank statements, and a complete list of your debts and assets. Pulling these documents together typically takes one to two weeks if you start promptly, and having them ready before your first attorney meeting shortens your overall timeline considerably.

Filing through discharge

Once you file, the court assigns a trustee and schedules your 341 meeting of creditors, usually three to five weeks out . At that meeting, the trustee asks you questions under oath about your finances. Creditors may attend but rarely do in straightforward consumer cases. After the meeting, creditors have 60 days to object to the discharge of specific debts.

If no objections are filed and the trustee finds no non-exempt assets to administer, the court issues your discharge shortly after that 60-day window closes.

You also must complete a debtor education course after filing but before your discharge is granted . That requirement typically takes two hours and can be completed online, so it rarely adds meaningful delay if you handle it early.

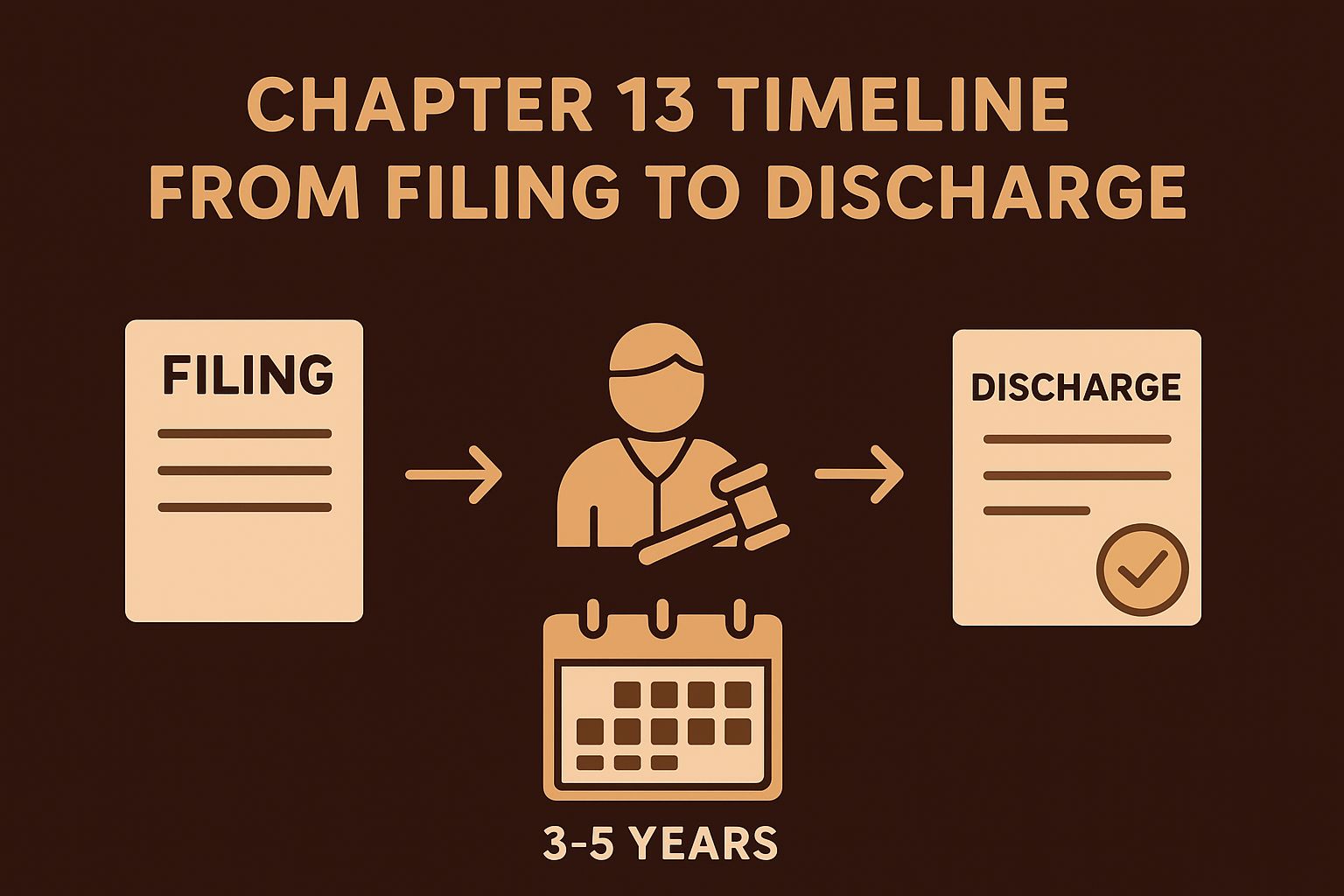

Chapter 13 timeline from filing to discharge

Chapter 13 answers the question of how long does bankruptcy take in a very different way than Chapter 7. Instead of a four-to-six-month process, you commit to a court-approved repayment plan lasting three to five years , during which you make monthly payments to a trustee who distributes funds to your creditors. The longer timeline reflects what Chapter 13 actually does: it gives you structured time to catch up on mortgage arrears, car loans, and other secured debts without losing the property attached to them.

From filing to plan confirmation

Once you file your petition and proposed repayment plan, the court schedules your 341 meeting of creditors three to five weeks later , following the same process as Chapter 7. After that meeting, creditors have an opportunity to object to your plan before the bankruptcy judge holds a confirmation hearing, typically 45 to 90 days after you file . The judge reviews your plan to confirm it meets legal requirements and that your proposed payments are realistic based on your income and expenses.

If creditors raise objections at the confirmation hearing, you may need to revise and resubmit your plan, which adds weeks to your timeline before the court approves it.

Completing the plan and reaching discharge

Your monthly payments run for either 36 or 60 months , depending on whether your income falls below or above the state median. During that period, you must stay current on all payments and continue filing your annual tax returns with the trustee. Once you complete every required payment and finish your debtor education course , the court issues your discharge, formally releasing you from remaining eligible balances on unsecured debts.

What can delay or speed up a case

If you want to understand how long does bankruptcy take in practice, it helps to know that the court's official schedule is only part of the equation. Your own actions before and after filing have a direct impact on whether your case moves efficiently or sits in a queue while issues get resolved. Two broad categories determine which direction your timeline goes: avoidable mistakes that create holdups, and deliberate steps that keep things moving.

Common causes of delay

Missing or incomplete paperwork is the most frequent source of delay in bankruptcy cases. If your petition contains errors, omits creditors, or uses incorrect income figures, the trustee will flag those issues and the court cannot move forward until you correct them. Creditor objections add another layer of uncertainty, particularly when a creditor challenges the dischargeability of a specific debt, because the court must schedule a hearing and resolve the dispute before your case can close.

A prior bankruptcy filing within a certain number of years can also limit or eliminate your automatic stay, which adds legal complications that require court action before your case proceeds normally.

Steps that move your case forward faster

Starting your credit counseling course before your first attorney meeting removes one scheduling dependency immediately. Gathering your last two years of tax returns, three to six months of bank statements, and a full list of creditors before your initial consultation means your attorney can prepare accurate paperwork from the start. Responding promptly to any requests from your trustee or attorney for additional documentation prevents the kind of back-and-forth that quietly stretches timelines by weeks.

Where to go from here

Now that you understand how long does bankruptcy take under each chapter, the next step is figuring out which path actually fits your income, your debts, and your financial goals. Chapter 7 offers a faster resolution in four to six months, while Chapter 13 gives you structured time to protect property and catch up on secured debts over three to five years. Neither option is universally better; the right choice depends entirely on your specific numbers and what you need to keep.

Getting that answer starts with a conversation. At Mayfield Law Firm, P.A., we offer free consultations for clients across Northeast Mississippi and South Memphis, and we've handled Chapter 7 and Chapter 13 filings for over 40 years. Bring your income information and a rough list of your debts, and we'll walk you through the means test, explain your realistic timeline, and help you take the next step with confidence.