Wage Garnishment Exemptions: What Income Is Protected

A creditor sues you, gets a judgment, and suddenly your paycheck shrinks before it even hits your bank account. That's when most people start searching for wage garnishment exemptions , usually after the first smaller check already stung. The good news is that federal and Mississippi law both limit how much a creditor can take, and some income can't be touched at all.

This article answers the question directly: which wages and benefits are protected, how much of your paycheck creditors can legally garnish, and what steps to take if you believe too much is being withheld. We'll walk through federal exemption limits under the Consumer Credit Protection Act, state-specific protections in Mississippi and Tennessee, and categories of income like Social Security and disability benefits that are largely off-limits to most creditors.

We'll also cover the claim of exemption process , the paperwork courts require, and realistic deadlines for filing before your next paycheck gets hit again. If garnishment is already squeezing your budget, this breakdown gives you the facts to act, whether that means filing an exemption or exploring bankruptcy protection through Mayfield Law Firm to stop collections for good.

Why wage garnishment exemptions matter

The real cost of losing a paycheck

Without limits on garnishment, a single judgment could wipe out most of your take-home pay in one pay period. Federal law steps in specifically to prevent that outcome, capping how much a creditor can pull from your wages so you still have enough left to cover rent, utilities, and groceries. If you've ever opened a paycheck stub and seen a chunk missing, you already know how fast that gap turns into missed bills or a bounced payment.

- Rent or mortgage payments fall behind

- Utility shutoffs become a real threat

- Car payments lapse, risking repossession

- Grocery and gas budgets shrink to nothing

Federal law sets the baseline

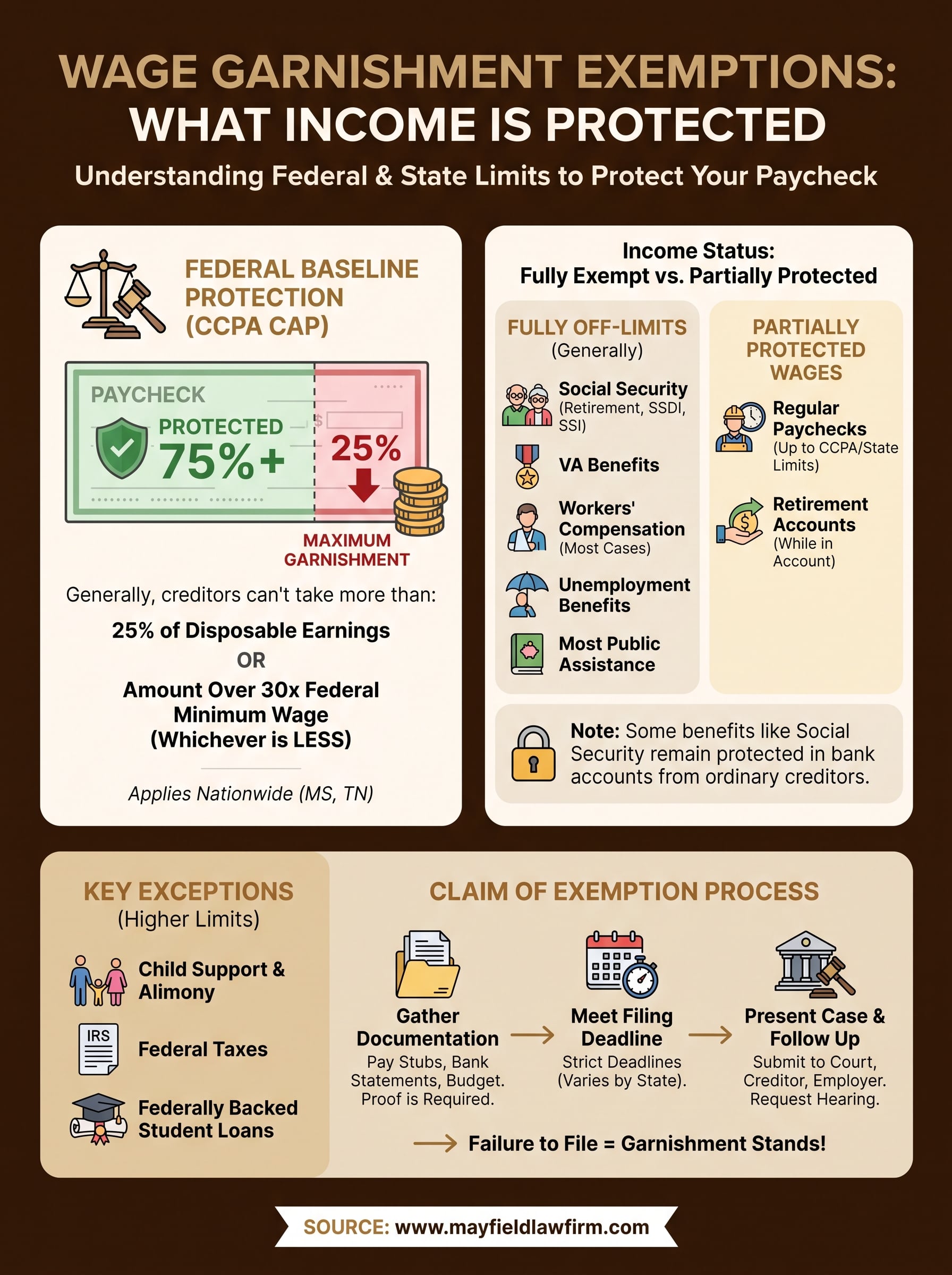

Under the Consumer Credit Protection Act (CCPA) , a creditor generally can't take more than 25% of your disposable earnings, or the amount by which your weekly wages exceed 30 times the federal minimum wage, whichever is less. This rule applies nationwide, including in Mississippi and Tennessee, and it's enforced by the U.S. Department of Labor. You can read the full breakdown directly from the Department of Labor's wage garnishment guidance. That 25% figure is a ceiling, not a guarantee, and creditors routinely garnish right up to that limit unless you assert an exemption.

Without a claimed exemption, a court assumes your entire paycheck is fair game up to the legal maximum.

Why the exemption process exists

Exemptions exist because Congress and state legislatures recognized that some income simply isn't meant to satisfy debt, whether it's a Social Security check, disability payment, or the last few hundred dollars standing between a family and eviction. Bankruptcy attorneys see this pattern constantly: someone assumes the garnishment amount is fixed and non-negotiable, when in reality a portion of it may be fully exempt under state or federal law. Knowing this distinction changes how you respond, because a garnishment that looks unstoppable might actually be reducible or reversible with the right paperwork.

Mississippi, like most states, layers additional protections on top of the federal floor, and some categories of income are exempt entirely regardless of the CCPA percentage. That's why understanding wage garnishment exemptions matters before you assume you have no options. Garnishment orders don't check your circumstances automatically. Courts rely on you, the debtor, to raise the exemption and prove it applies. Miss that step, and the maximum legal amount keeps coming out of every check until the judgment is satisfied or you take action to stop it.

Which income sources are commonly exempt

Most people assume every dollar they earn is up for grabs once a judgment hits, but that's not true. Federal and Mississippi law both carve out specific categories of income that creditors can't touch, no matter how large the debt. Recognizing which of your income streams fall into this protected category is the first step toward stopping an overly aggressive garnishment.

Benefits that are fully off-limits

Several types of government benefits carry automatic protection from most creditors, meaning they're exempt whether or not you file paperwork. Social Security retirement, SSDI, and SSI payments top this list, along with VA benefits and most public assistance. The Social Security Administration confirms this protection directly in its own garnishment guidance. Ordinary judgment creditors, like credit card companies or medical debt collectors, generally can't garnish these funds even after they land in your bank account.

Social Security and disability benefits stay protected from ordinary creditors even after they hit your bank account.

Wages that carry partial protection

Regular paychecks don't get blanket immunity, but the CCPA cap and Mississippi's own exemption rules limit how much a creditor can reach. Below is a quick reference for common income types:

| Income Source | Exemption Status |

|---|---|

| Social Security/SSDI/SSI | Fully exempt from ordinary creditors |

| VA disability benefits | Fully exempt |

| Workers' compensation | Exempt in most cases |

| Unemployment benefits | Exempt from most creditors |

| Regular wages | Protected up to CCPA/state limit only |

| Retirement accounts (401k, pensions) | Generally exempt while in the account |

Exceptions worth knowing

These protections shrink for specific debts. Child support, alimony, federal taxes, and federally backed student loans all carry higher garnishment ceilings and can reach income that's otherwise shielded. If your garnishment stems from one of these sources, don't assume the same exemption rules apply, because they often don't.

How to file a claim of exemption

Once you know which income qualifies, the next step is putting that protection on paper. Filing a claim of exemption tells the court, in writing, that some or all of the money being garnished falls outside what a creditor can legally take. Skip this step and the garnishment order stands as written, even if your paycheck includes exempt Social Security deposits or falls below the CCPA threshold.

Gather your documentation

Courts want proof, not just an assertion, so start collecting records before you file anything.

- Recent pay stubs showing gross and net wages

- Bank statements identifying exempt deposits like SSDI or SSA payments

- A household budget showing rent, utilities, and other fixed costs

- A copy of the garnishment order or writ you received

- Any prior court judgment tied to the debt

Meet the filing deadline

Every state sets its own window, and Mississippi courts typically give you a short period, often measured in days, to respond after the garnishment notice arrives. Missing that deadline usually means the garnishment continues unchallenged for the full pay period, sometimes longer, and reversing it retroactively is far harder than filing on time.

A missed deadline is often the only reason a valid exemption never gets applied.

Present your case and follow up

Submit your completed exemption claim to the court that issued the garnishment, along with copies to the creditor and your employer's payroll department. Request a hearing if the court doesn't automatically schedule one, since some clerks require you to ask directly rather than assume it's already on the calendar. Following through matters just as much as filing correctly, because courts won't chase down missing paperwork on your behalf, and an incomplete claim of exemption often gets denied by default rather than approved on a technicality.

How exemption rules can vary by state

Federal law sets a floor, not a ceiling, which means Mississippi and Tennessee can each layer on their own protections beyond the CCPA's 25% cap. State-specific exemptions often catch people off guard, especially those who moved across the state line or work in one state while living in another. Since Mayfield Law Firm serves clients in both Southaven and Memphis, understanding how these two neighboring states differ matters more than it might in a single-state practice.

Mississippi's approach to garnishment

Mississippi generally follows the federal CCPA limits without adding many extra layers, though it does exempt certain public benefits and a modest amount of personal property under its own exemption statutes. Judgment creditors in Mississippi still can't exceed the 25% federal ceiling, but state courts handle the claim of exemption process through the same court that issued the underlying judgment, so filing location matters as much as filing timing.

Tennessee's additional protections

Tennessee builds in a head-of-household exemption that can shrink the garnishable amount even further for debtors supporting a spouse or dependent children. This protection isn't automatic. You have to claim it, and Tennessee courts require documentation proving dependents actually rely on your income.

The same paycheck can face different garnishment limits depending on which side of the state line issued the judgment.

| Factor | Mississippi | Tennessee |

|---|---|---|

| Federal CCPA cap | Applies | Applies |

| Head-of-household exemption | Not standard | Available with proof of dependents |

| Filing location | Court that issued judgment | Court that issued judgment |

| Extra state exemptions | Limited | Broader for family income |

Why cross-border cases get complicated

Residents who live in Mississippi but earn wages in Tennessee, or vice versa, sometimes face conflicting guidance from employers unfamiliar with dual-state rules. Cross-border garnishment cases benefit from local counsel who already knows which court has jurisdiction and which state's protections actually apply to your specific paycheck.

Protecting your paycheck going forward

Garnishment feels permanent until you realize how much of it depends on paperwork you haven't filed yet. Wage garnishment exemptions exist precisely because lawmakers knew a paycheck can't be squeezed dry without consequences for the whole household. Once you know which income qualifies, whether it's Social Security, disability pay, or a portion of your regular wages under the CCPA cap, the path to reducing or stopping the garnishment becomes a lot clearer.

Don't wait for a second smaller check to confirm what you already suspect. Pull your pay stubs, check your state's deadlines, and file your claim before the next withdrawal happens. If the garnishment ties back to debt that bankruptcy could resolve entirely, that's worth exploring too. Schedule a free consultation with Mayfield Law Firm and find out which protections apply to your paycheck and your situation.