Wage Garnishment Rights: Limits, Exemptions, And Protections

Finding out that a portion of your paycheck is about to be, or already is, taken before it even reaches your bank account is stressful. Wage garnishment rights exist to prevent creditors from taking everything, but most people don't learn about these protections until they're already losing money. Federal and state laws set strict limits on how much can be withheld from your earnings, and certain types of income are off-limits entirely.

At Mayfield Law Firm, P.A., we help clients across Northeast Mississippi and South Memphis who are dealing with debt-related legal issues, including garnishments tied to unpaid debts . Through our bankruptcy practice, we've seen firsthand how garnishment can push families to a financial breaking point, and how the right legal action can stop it in its tracks .

This article breaks down the federal and state rules that govern wage garnishment, explains which income sources are exempt, outlines your protections against employer retaliation, and walks through the legal options available to you if a creditor is already garnishing your wages. Whether you're trying to prevent garnishment or stop one that's already started, understanding your rights is the first step .

Why wage garnishment rights matter

Most people assume that once they earn money, it belongs to them. But when a court or government agency issues a garnishment order, your employer is legally required to withhold a portion of your wages and send it directly to a creditor before you ever see it. Understanding your wage garnishment rights is not optional background knowledge - it is practical protection that directly affects how much money you take home every pay period.

The financial impact on your household budget

A garnishment does not reduce your paycheck by a small, manageable amount. Federal law under the Consumer Credit Protection Act caps how much a creditor can take, but even the maximum allowable amount can make it nearly impossible to cover rent, utilities, groceries, and other monthly bills. Families living paycheck to paycheck feel this pressure immediately, sometimes within the first pay cycle after a garnishment begins.

Things become more complicated when multiple creditors pursue garnishment at the same time, or when a government agency like the IRS initiates a levy for unpaid taxes. Tax garnishments carry different, and often more aggressive, limits than ordinary consumer debt. Without knowing exactly which rules apply to your situation, you may not realize a creditor is taking more than the law allows.

If a garnishment is causing you to fall behind on basic living expenses, that is a signal to get legal advice as quickly as possible.

How garnishment affects more than just your paycheck

Beyond the direct financial hit, wage garnishment creates a chain of secondary problems that can follow you for months. Late payments on other bills, damage to your credit score, and the stress of ongoing financial instability all compound the original issue. Your employer is also notified directly when a garnishment order arrives, which adds a layer of workplace stress that many people are not prepared for.

Federal law does provide limited job protection: under the CCPA, an employer cannot fire you solely because one creditor has garnished your wages. However, that protection does not extend to situations where two or more separate creditors garnish your wages at the same time. Knowing this distinction matters, because it affects how quickly you need to respond to a garnishment notice. Waiting often allows the garnishment to continue longer than necessary, and the longer it runs, the more ground you lose financially.

How wage garnishment works in the real world

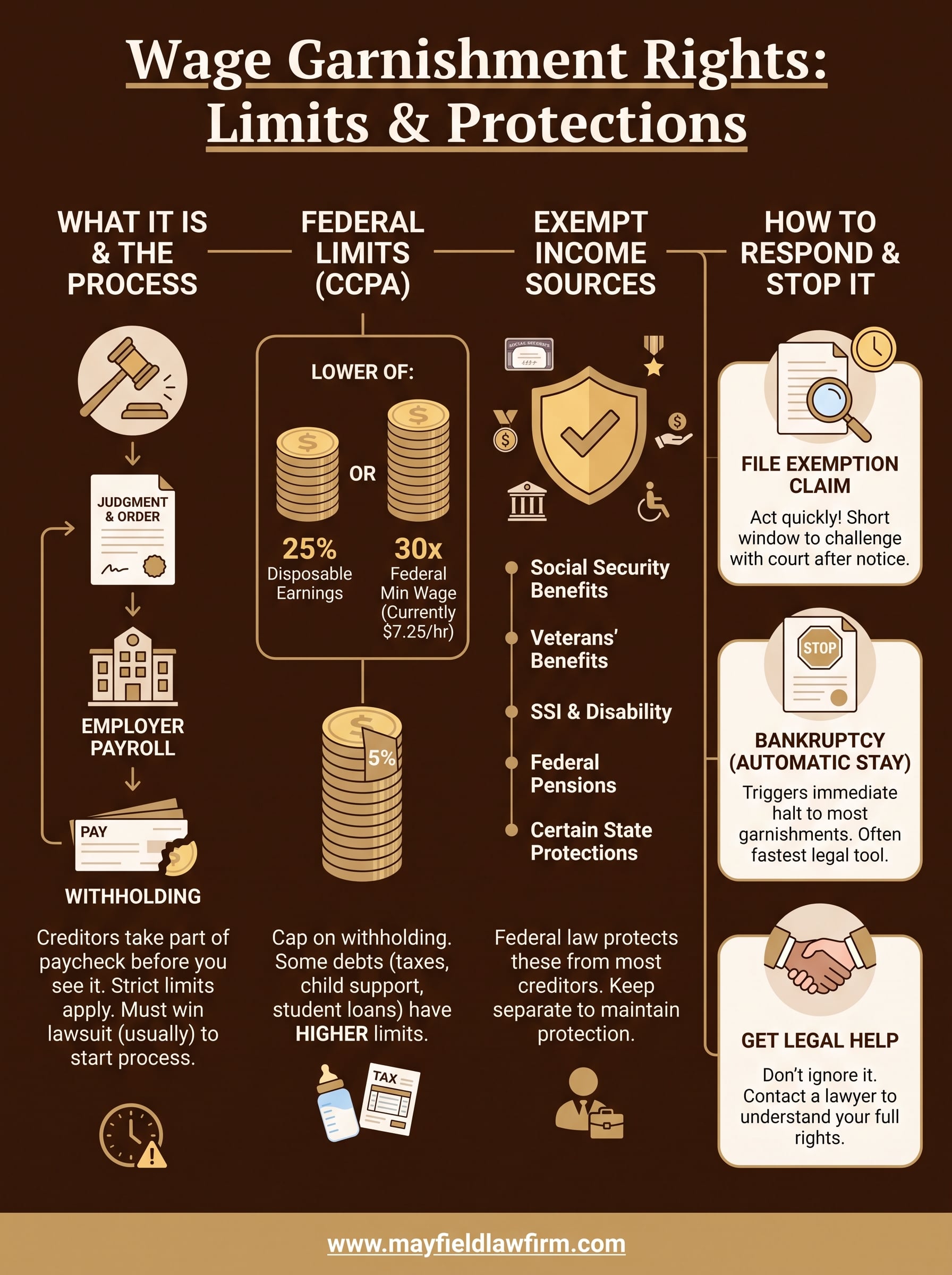

Wage garnishment does not happen without warning, but it can feel that way if you are not familiar with the process. In most cases, a creditor must first file a lawsuit, win a judgment against you, and then apply to the court for a garnishment order before they can touch your paycheck. Government agencies like the IRS or a state child support enforcement office can bypass the lawsuit step entirely, which is one reason tax levies and support garnishments often feel more abrupt and harder to stop.

How a garnishment order reaches your employer

Once a court issues a garnishment order, it goes directly to your employer's payroll department , not to you. Your employer receives legal instructions requiring them to withhold a specific percentage of your disposable earnings each pay period. They have no choice but to comply. Failing to follow the order exposes your employer to legal penalties , so the process typically starts by the very next paycheck after the order arrives.

You should receive a copy of the garnishment order as well, usually by mail. That notice is your window to act. Many people set it aside or ignore it, which is a costly mistake. Your wage garnishment rights include the ability to challenge the garnishment through a court exemption claim, but most states give you only a short period, sometimes as little as ten days, to file one after receiving notice.

The moment you receive a garnishment notice, the clock starts. Acting quickly gives you the best chance of reducing or stopping the withholding before your next paycheck is affected.

When garnishment continues without action

If you take no action, the garnishment runs until the full debt is paid , including any interest and court costs the creditor has added. Some garnishments last months. Others stretch on for years , draining your income long after you may have assumed the debt was behind you.

How much of your wages can be garnished

Federal law sets the baseline for how much a creditor can take from each paycheck. Under the Consumer Credit Protection Act, the garnishment amount is capped at whichever is lower : 25% of your disposable earnings, or the amount by which your disposable earnings exceed 30 times the federal minimum wage (currently $7.25 per hour). Disposable earnings are what remains after legally required deductions like taxes and Social Security are withheld.

Federal limits under the CCPA

The federal minimum wage calculation matters more than many people realize. If you earn close to minimum wage , the 30x rule may protect a larger share of your paycheck than the 25% cap would. For example, if your disposable weekly earnings are $250, then 30 times $7.25 equals $217.50, and the difference is only $32.50. That means a creditor could garnish just $32.50 per week under that calculation, far less than 25% of $250, which would be $62.50.

Knowing which calculation applies to your specific pay period can mean the difference between covering your rent and falling short.

Mississippi follows federal garnishment limits for most consumer debts, so your wage garnishment rights in this state align closely with the federal floor. If a creditor is taking more than these caps allow, that is a legal violation you can challenge directly in court.

When higher limits apply

Not all garnishments follow the standard 25% cap. Child support and alimony garnishments can reach up to 50% of your disposable earnings if you currently support another spouse or child, and up to 60% if you do not. Federal tax levies issued by the IRS follow a separate formula based on your filing status and number of dependents, which can result in significantly larger withholdings. Federal student loan garnishments can reach up to 15% of disposable earnings without requiring a court judgment first.

What income and pay types may be protected

Not every dollar you receive is automatically fair game for garnishment. Federal law shields several categories of income from creditor reach entirely, and your state may layer on additional protections depending on where you live and how much you earn. Understanding which income types fall outside a creditor's reach is a critical part of knowing your wage garnishment rights .

Federal exemptions for certain income sources

Federal law places strong protections on government benefit payments. If you receive Social Security retirement or disability benefits, Supplemental Security Income (SSI), veterans' benefits, federal pension income, or disability compensation , those funds cannot be garnished by most ordinary creditors. Child support and alimony obligations are exceptions, as are federal tax debts, but even those carry limits.

If exempt funds are deposited into a bank account, federal rules require banks to automatically protect a minimum of two months' worth of those benefit payments from being frozen or seized.

The protections become more complicated once exempt income mixes with other funds in a single bank account. Keeping benefit payments in a separate account with no other deposits is the cleanest way to maintain the paper trail that shows which money is legally protected.

Pay types that may receive added protection in Mississippi

Mississippi follows federal garnishment limits, but certain lower-income earners may find the 30x federal minimum wage formula provides meaningful protection even beyond what the standard 25% cap would allow. Workers who rely on tips, commissions, or irregular pay should note that the same federal rules apply to their total disposable earnings per pay period, not just their base hourly wage. If tips push your total disposable earnings higher one week, a creditor can garnish based on that higher figure. Tracking your actual pay each cycle gives you the information you need to verify that your employer is withholding the correct amount and nothing more.

How to respond and protect your paycheck

When a garnishment order arrives, you have more options than most people realize, but acting quickly is essential . Your wage garnishment rights include the ability to formally challenge a garnishment through the court system, negotiate directly with the creditor in some cases, or use federal bankruptcy protections to stop the withholding entirely. Doing nothing guarantees the garnishment continues.

File an exemption claim immediately

Most courts give you a narrow window after you receive a garnishment notice to file a claim of exemption , which is a formal request asking the court to recognize that some or all of your income falls under a protected category. You fill out a form, specify which exemptions apply to your situation, and submit it before the deadline. Missing that window typically means you lose the right to challenge the garnishment , at least until circumstances change.

If you receive any of the federally protected income types discussed earlier, like Social Security benefits or veterans' compensation , document that clearly on your exemption form. Courts take these claims seriously, and a well-supported exemption request can result in a full or partial reduction of the garnishment almost immediately.

Use bankruptcy to stop garnishment fast

Filing for bankruptcy triggers what is known as an automatic stay , which is a court order that immediately halts most garnishments the moment your case is filed. This applies to both Chapter 7 and Chapter 13 bankruptcy , and it takes effect before your case is even reviewed. For many people dealing with aggressive creditor collection, this is the fastest legal tool available to stop the bleeding.

A bankruptcy filing does not resolve every garnishment permanently, but it buys you time and legal protection to work out a sustainable path forward.

Chapter 13 in particular allows you to restructure the underlying debt that triggered the garnishment, which addresses the root problem rather than just pausing the symptoms.

Your next move

Wage garnishment rights give you real legal tools to fight back, but those tools only work if you use them before the window closes. If a creditor is already taking money from your paycheck, or if you received a notice and are not sure what to do with it, the worst move is to wait. Every pay period you delay is money you do not get back.

Bankruptcy is often the fastest and most effective way to stop a garnishment immediately, and it also addresses the underlying debt that caused the problem. Mayfield Law Firm, P.A. has helped clients across Northeast Mississippi and South Memphis stop garnishments, protect their income, and build a real path out of debt. The firm offers free consultations, so there is no cost to find out exactly where you stand.

Contact Mayfield Law Firm, P.A. today to talk through your situation and find out what legal steps are available to you.