How Does Wage Garnishment Work? The Process Explained

Opening your paycheck and finding a chunk missing is a gut punch, especially when you didn't sign off on it. If you're asking how does wage garnishment work , you're probably staring at a court notice or a smaller deposit than usual, and you need answers fast, not legal theory.

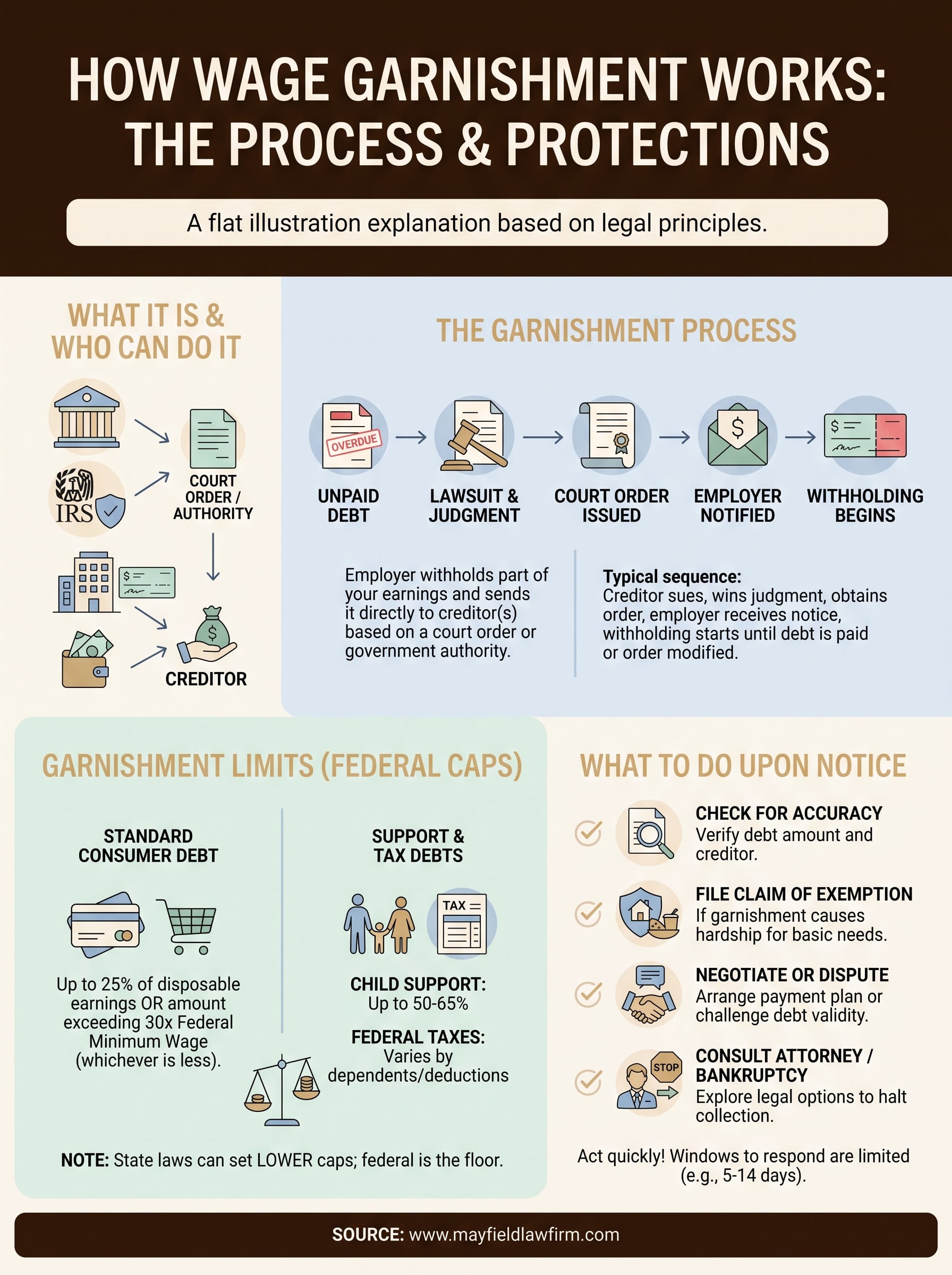

Here's the short version: wage garnishment happens when a creditor gets a court order (or, in cases like tax debt, skips that step entirely) directing your employer to withhold part of your earnings and send it straight to them. Federal and state law cap how much can be taken, and certain debts, like child support or unpaid taxes, follow different rules than credit card debt. Your employer can't fire you over a single garnishment either, though that protection has limits.

In this article, we'll walk through the entire process step by step: how creditors get approval to garnish, how much of your paycheck is actually protected , and what options you have to stop or reduce a garnishment before it drains your income for months on end.

Why wage garnishment matters for your paycheck and rights

Wage garnishment matters because it changes your monthly budget without asking your permission first. Once a garnishment order lands on your employer's desk, your take-home pay shrinks before you even see it, and that shortfall has to come from somewhere else, whether that's rent, groceries, or your car payment. Understanding your rights now, before a notice ever arrives, puts you in a much stronger position to react quickly instead of scrambling.

The immediate financial squeeze

Missing even 15% of your paycheck for months at a time can push a household from stable to struggling fast. A single garnishment order rarely covers just one pay period; it typically continues until the debt is paid off or a court modifies it, which means the hit repeats every payday. Families already living paycheck to paycheck often find themselves choosing between utility bills and car repairs once the withholding starts.

A wage garnishment doesn't just take money once, it reshapes your budget for as long as the order stays active.

Not all debts follow the same rules

Federal law treats debts differently depending on what you owe and to whom. Some creditors need a court judgment before they can touch your paycheck, while government agencies like the IRS can bypass that step entirely under federal authority. Knowing which category your debt falls into tells you how much leverage you actually have to fight back.

| Debt type | Court order required? | Typical garnishment cap |

|---|---|---|

| Credit card or medical debt | Yes | Up to 25% of disposable earnings |

| Federal student loans | No | Up to 15% of disposable earnings |

| Unpaid federal taxes | No | Varies by dependents and deductions |

| Child support or alimony | No | Up to 50-65% of disposable earnings |

The U.S. Department of Labor outlines these limits under Title III of the Consumer Credit Protection Act, which sets the federal floor every state must follow.

Your job and rights don't disappear

Your employer cannot fire you for a single wage garnishment, no matter how uncomfortable the paperwork feels for the payroll department. That protection comes directly from federal law, though it only covers one garnishment order; a second one tied to a different debt can strip that safety net away. Beyond job security, you keep several other rights the moment a garnishment starts:

- The right to receive written notice before withholding begins

- The right to claim exemptions that protect a portion of your income

- The right to dispute the debt or the garnishment amount in court

- The right to request a hardship exemption if the garnishment leaves you unable to cover basic living expenses

Recognizing these protections early is often what separates someone who negotiates a manageable resolution from someone who loses months of income to a debt they could have challenged.

How the wage garnishment process actually works

Getting from an unpaid debt to an actual garnishment order takes several legal steps, and skipping any of them usually means the creditor can't touch your paycheck yet. Most creditors can't just call your boss and ask for money; they have to earn that right through the courts first, unless they're a government agency with special authority.

The lawsuit and judgment stage

Before a private creditor, like a credit card company or medical provider, can garnish your wages, they typically have to sue you and win a court judgment . That means filing a lawsuit, serving you with notice, and either winning a default judgment because you didn't respond or winning after a hearing. Once the judgment is entered, the creditor requests a garnishment order (sometimes called a writ of garnishment) from the court, which then gets delivered to your employer.

Once a court judgment exists, your employer becomes legally obligated to withhold your wages, whether you agree with the debt or not.

What happens once your employer gets the order

Your employer doesn't get a choice once a valid garnishment order arrives. Payroll calculates your disposable earnings , applies the correct withholding percentage, and sends that portion directly to the creditor or court on every pay cycle. Here's the typical sequence from start to finish:

- Creditor obtains a court judgment (or bypasses this step for taxes and student loans).

- Creditor requests a garnishment order from the court.

- Court issues the order and serves it to your employer.

- Employer notifies you in writing of the garnishment.

- Payroll begins withholding the legally permitted amount starting the next pay period.

- Withholding continues until the debt is satisfied or a court modifies the order.

Seeing the process laid out this way makes one thing clear: by the time money disappears from your check, several legal checkpoints have already passed. That's exactly why acting the moment you receive a lawsuit notice, rather than waiting for the garnishment itself, gives you the best shot at stopping it before it starts.

How much of your wages can legally be garnished

Federal law sets a hard ceiling on how much a creditor can pull from your paycheck, and that ceiling depends on your disposable earnings , not your gross pay. Disposable earnings are what's left after mandatory deductions like taxes and Social Security, not after voluntary deductions like retirement contributions or health insurance. Creditors can't just take a flat percentage of your salary; the law forces a specific calculation every pay period, and getting that math wrong is one of the most common payroll mistakes that leaves workers underpaid or overpaid.

The federal 25% rule

Under Title III of the Consumer Credit Protection Act, standard creditors can garnish the lesser of 25% of your disposable earnings or the amount by which your weekly wages exceed 30 times the federal minimum wage. This dual-cap formula exists specifically to protect low-wage workers from losing their entire paycheck to a single garnishment order , since someone earning minimum wage could otherwise be left with almost nothing to live on.

No matter how large the debt, federal law protects a baseline amount of income that a creditor can never touch.

Special rules for support and tax debt

Child support and alimony orders operate outside that 25% ceiling entirely. Depending on whether you're already supporting another family and how far behind you are on payments, up to 50% to 65% of your disposable earnings can be withheld. Unpaid federal taxes follow their own formula too, one based on your filing status and number of dependents rather than a flat percentage, which the IRS publishes annually and updates as tax brackets shift.

State laws can lower your cap further

States sometimes set stricter garnishment limits than federal law requires, and whichever cap is lower, federal or state, is the one that actually applies to your paycheck. Mississippi and Tennessee both generally follow the federal 25% standard for consumer debt, but confirming the details with a local attorney matters since exemptions and homestead protections vary by state and can change how much of your income stays untouched from creditors.

What to do if you receive a wage garnishment notice

Receiving a wage garnishment notice feels like the ground shifting under you, but panic wastes time you don't have. Every state gives you a limited window, often just five to fourteen days, to respond before withholding begins, so acting fast matters more than acting perfectly. Reading the notice carefully first tells you who's garnishing, how much, and which court issued the order.

Check the notice for accuracy

Start by verifying the debt actually belongs to you and the amount matches what you owe. Mistaken identity and outdated balances happen more often than people expect, especially with debts that have been sold to collection agencies multiple times. If something looks wrong, you can challenge the garnishment order in court before money ever leaves your paycheck.

The fastest way to lose a fight against garnishment is to assume the notice is correct without checking it.

Know your options before withholding starts

You generally have several paths open once a notice arrives, and each one changes the outcome differently:

- File a claim of exemption if the garnishment would leave you unable to cover rent, food, or utilities.

- Negotiate directly with the creditor for a payment plan that avoids garnishment altogether.

- Dispute the underlying debt if you believe it's inaccurate, already paid, or past the statute of limitations.

- Consult a bankruptcy attorney if garnishment is one of several debts overwhelming your income, since filing can trigger an automatic stay that halts collection.

Talk to your employer

Your payroll department has to comply with a valid order, but that doesn't mean they're your enemy in this. Letting your employer know you're actively disputing or resolving the debt keeps communication open and avoids surprises on payday. Employers deal with garnishments regularly, so most won't treat a single order as a red flag against you.

Waiting until the withholding starts to explore these options usually means losing income you could have protected. The sooner you respond to a wage garnishment notice, the more control you keep over what happens to your paycheck next.

Moving forward after a garnishment order

Wage garnishment feels permanent when it starts, but it isn't. Once you understand the court process behind it, the withholding caps that protect your paycheck, and the specific steps you can take after a notice arrives, you have real leverage instead of just anxiety. Every option, from claiming a hardship exemption to negotiating directly with the creditor to filing bankruptcy, works best when you act before withholding begins rather than after.

If you're staring down a garnishment notice right now in Mississippi or Memphis, don't wait to see how much of your next check disappears. A local attorney can review the judgment, check whether the amount matches what the law allows, and tell you honestly whether fighting it, negotiating it, or filing for bankruptcy protection makes the most sense for your situation. Schedule a free consultation with Mayfield Law Firm and find out what your next paycheck could actually look like.