Debt Collector Calling Family Members: Is It Legal?

Your phone stops ringing, but now your sister's does. Or your elderly mother gets a call from someone asking about a debt that isn't even hers. If a debt collector calling family members in your life has you worried or angry, you're not imagining a problem. This happens more often than most people realize, and it leaves families confused about what's actually allowed.

Here's the short answer: collectors can contact your relatives, but only under strict limits , and almost always just once, to track down your address or phone number. They generally cannot discuss your debt, demand payment from a family member, or call repeatedly once they've gotten what they need. The Fair Debt Collection Practices Act (FDCPA) spells out exactly what's off limits, and violations happen more than you'd think.

Below, we break down what the law permits, what crosses the line into harassment, and the concrete steps you can take to make it stop. If a collector has already violated your rights or your family's, you'll also find out when it's worth talking to an attorney about recourse.

Why debt collectors contact family members at all

Debt collectors reach out to relatives for one main reason: they can't find you, or they think a family member might pressure you into paying faster than a letter would. When a collection agency buys or takes on an old account, the contact information on file is often outdated. Maybe you moved, changed your number, or the debt is years old and the original creditor's records are stale. Rather than give up, collectors turn to a legal tool called "skip tracing" , which means using public records, old applications, and sometimes family connections to locate you.

Skip tracing and why it's legal in a narrow sense

Skip tracing itself isn't illegal. Under the FDCPA, a collector is allowed to contact people other than the debtor for the specific purpose of gathering location information , meaning your address, home phone number, or place of employment. This is often called a "third-party contact," and the law permits it because Congress recognized that collectors sometimes have a legitimate need to find someone who owes money and has become unreachable.

A debt collector can call your family to find you, but not to collect from them.

Here's what a legitimate location-information call is supposed to look like:

- The collector identifies themselves and their employer, but doesn't have to say they're a debt collector.

- They ask only for your address, phone number, or employer, nothing about the debt itself.

- They don't reveal that you owe money or discuss any details of the account.

- They contact each person, in most cases, only once, unless they have a specific reason to believe the earlier information was wrong or incomplete.

If the call sticks to that script, the collector is operating within the law, even if it feels invasive to the family member receiving it.

When it crosses from tracking down to pressure tactics

The trouble starts when collectors use that first legal contact as a doorway to something else. Some agencies call a sibling, parent, or adult child repeatedly, hoping that family pressure will get the debt paid faster than legal notices would. Others use vague or alarming language, like implying legal trouble is imminent, so that whoever answers the phone feels compelled to track you down or even offer to pay on your behalf.

This tactic isn't new, and it isn't rare. The Consumer Financial Protection Bureau has fielded thousands of complaints over the years involving collectors who disclosed debts to relatives, called repeatedly after getting the needed information, or used deceptive framing to make family members believe they were personally responsible. You can see the scope of these complaints in the CFPB's own consumer complaint database, which tracks patterns across the collection industry.

Why some collectors gamble on aggressive tactics anyway

Collection agencies operate on volume. Many buy debt portfolios for pennies on the dollar and recover a profit even if only a fraction of accounts pay up. That business model creates an incentive to push boundaries, because most consumers don't know their rights well enough to push back, and even fewer file formal complaints. A collector calling your mother five times in a week is betting that the discomfort alone will produce results, whether that's your callback or her paying something just to make the calls stop.

Understanding this motivation matters, because it reframes what's happening. This usually isn't a mistake or a misunderstanding on the collector's side. It's often a calculated decision to test how far they can go before someone objects loudly enough, whether that's you filing a complaint or a lawyer sending a formal letter. Knowing that upfront changes how you respond. Instead of assuming the collector will stop once they realize they've overstepped, you should treat repeat contact with family as a signal that you need to act, document what happened, and put a stop to it using the tools the law gives you.

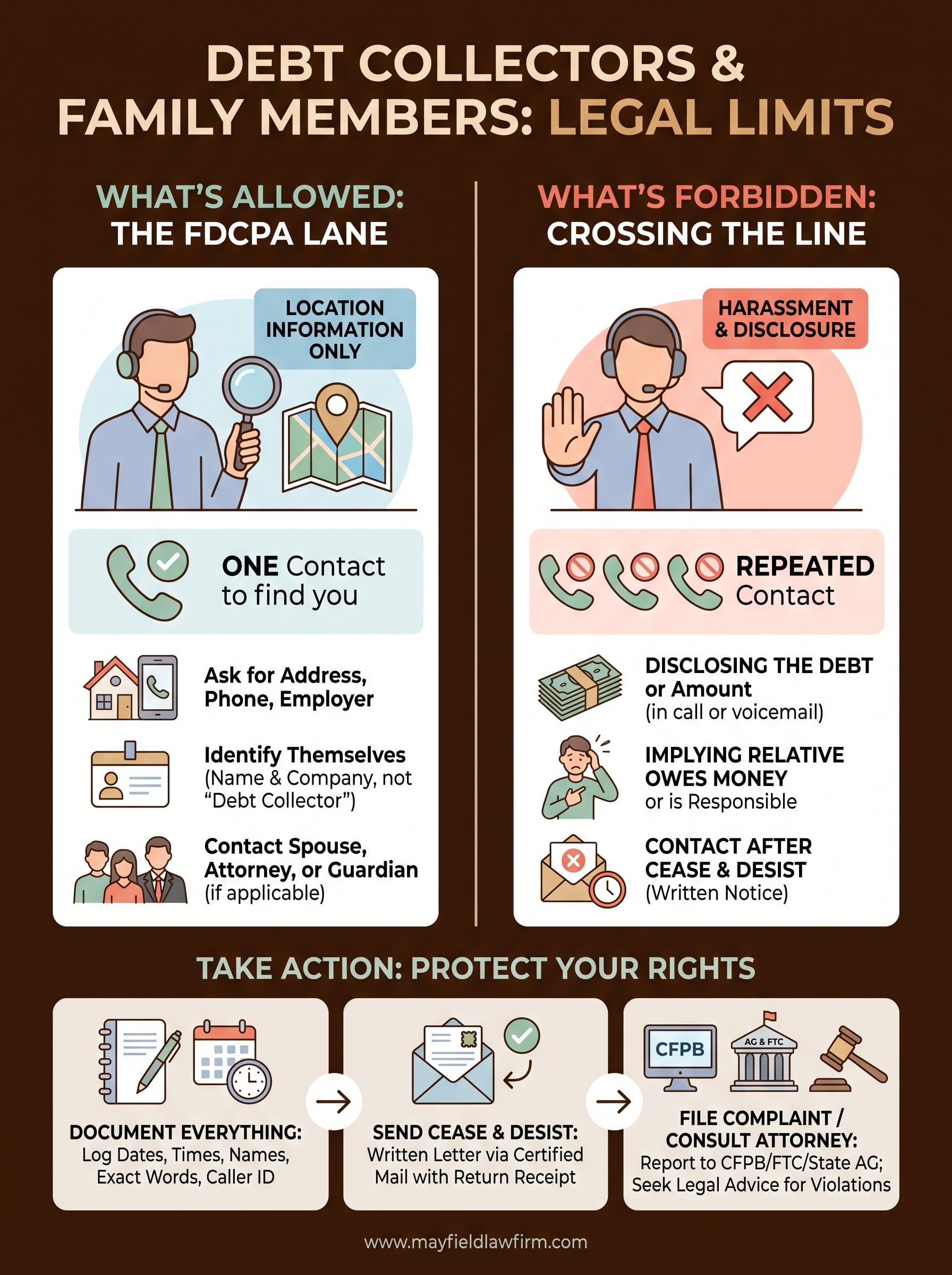

What the FDCPA actually allows and forbids

The Fair Debt Collection Practices Act draws a sharp line between finding you and pressuring your relatives to pay. Section 804 of the law covers exactly what a collector can say when they reach a third party, and Section 805 covers what happens once they've made contact with you directly. Together, these sections spell out a narrow lane for family contact, and almost everything outside that lane counts as a violation.

What's actually allowed

Collectors get one legitimate purpose for calling your family: gathering location information . Beyond that single goal, the law shuts the door.

- Asking a relative for your current address, phone number, or workplace

- Identifying themselves by name, and their employer's name if asked, without stating they work in debt collection

- Making a second attempt only if the first answer seems outdated or incorrect

- Contacting your attorney instead of you, if you've hired one

What's forbidden

Once a collector strays from location-gathering into anything resembling debt discussion, they've crossed into territory the FDCPA explicitly bans. The Consumer Financial Protection Bureau enforces these rules and treats them as bright lines, not suggestions.

| Forbidden practice | What it looks like in real life |

|---|---|

| Disclosing the debt | Telling your brother you owe $4,000 on a credit card |

| Repeated contact | Calling your mother three times after she's already given your number |

| Implying the relative owes money | Suggesting your spouse or adult child is responsible for payment |

| Contacting your employer about the debt | Calling your workplace and mentioning collections to a coworker |

| Using deceptive threats | Claiming a lawsuit or arrest is coming if the family doesn't help track you down |

| Contact after a cease-and-desist | Continuing to call relatives after you've sent written notice to stop |

Once a collector discusses your debt with anyone but you, your spouse, or your attorney, they've broken the law.

Why the details matter more than they seem to

The line between legal and illegal often comes down to a single sentence. A collector who says "I'm trying to reach John about a personal matter, can you give me his number" is inside the law. One who says "I'm trying to reach John about his overdue loan" has already violated it, even in that one sentence. This distinction trips up a lot of consumers, because the calls can sound similar on the surface, polite, brief, professional, while one is legal and the other opens the door to a claim.

Documenting exactly what was said matters here more than almost anything else you can do. If your family member remembers specific wording, especially anything mentioning the debt, an amount, or a threat, write it down immediately with the date, time, and caller's name if given. That record becomes the foundation for everything that follows, whether it's a cease-and-desist letter, a CFPB complaint, or a conversation with an attorney about damages under the FDCPA.

How to respond when a collector contacts your family

When a relative tells you a collector called, your first move should be calm information-gathering, not panic. Ask them exactly what was said, who called, what number showed up, and whether the caller named the debt or just asked for your contact information. Getting these details right away matters because memories fade fast, and a detailed record is what turns a vague complaint into a solid legal claim later.

Coach your family member before the next call

Give your relatives a short script they can use if the collector calls again. Most people freeze up on these calls or feel obligated to explain your business, so a few rehearsed lines make a real difference.

- "I'm not able to discuss anyone else's financial matters. Please don't call this number again."

- "Please send a letter instead of calling."

- "I'm hanging up now."

They don't owe the caller an explanation, an apology, or even a polite conversation. Ending the call quickly protects them from accidentally confirming information the collector can use, like your work schedule or a new phone number.

Don't let a relative pay on your behalf

Some families, especially older parents, feel pressured to offer money just to make the calls stop. Tell them directly: they are not responsible for your debt, and paying anything creates real complications, including reviving debt that might otherwise be past the statute of limitations. A collector who suggests a relative should pay, or even hints that it would help you, is misrepresenting the law.

No family member is legally required to pay your debt, no matter what a collector implies.

Document everything as it happens

Build a simple log the moment you learn about contact with your family. This record becomes essential if you send a cease-and-desist letter or file a complaint down the line.

Date:

Time:

Caller's name (if given):

Company name (if given):

Phone number that called:

Who received the call:

What was said (word for word if possible):

Was the debt mentioned? Y/N

Was payment demanded from the relative? Y/N

Keep this log updated with every incident, even ones that seem minor. A single call asking for your address might look harmless on its own, but a pattern of five calls over three weeks tells a very different story to the CFPB or a court.

Reach out to the collector yourself

Once you know a collector is contacting relatives, consider calling or writing the agency to confirm you've received their message and to redirect all future contact to you directly. This step isn't required, but it removes any excuse the collector has for continuing to call family, and it puts your objection in writing if you send it by email or letter rather than phone. From there, you're in a strong position to send something more formal if the contact doesn't stop, which is exactly what a cease-and-desist letter is built to do.

How to stop the calls with a cease-and-desist letter

A cease-and-desist letter is the single most effective tool you have under the FDCPA, because Section 805(c) requires a collector to stop nearly all contact once they receive one in writing. Written notice carries legal weight that a phone call never will, and it creates a paper trail showing exactly when the collector was put on notice. Send one as soon as you've confirmed a collector is reaching out to relatives, especially if the calls have continued past a single request for your address.

What the letter needs to say

Keep the letter short, factual, and specific. Vague language gives a collector room to argue they didn't understand what you wanted stopped.

[Your name]

[Your address]

[Date]

[Collection agency name]

[Collection agency address]

RE: Account number [if known]

To whom it may concern,

Under Section 805(c) of the Fair Debt Collection Practices Act, I am requesting that you cease all further communication with me and with any third party, including family members, regarding this account.

On [date], your company contacted [relative's name] at [phone number] and [briefly describe what happened, e.g., "disclosed that I owe a debt" or "called a second time after already receiving my contact information"].

Any further contact with me or my family outside what is legally permitted will be documented and may result in a formal complaint.

Sincerely,

[Your signature]

[Your printed name]

Send it the right way

Mail matters more than method here. Certified mail with return receipt gives you proof the collector received your letter and on what date, which becomes critical if they violate it later.

- Send the letter certified mail, return receipt requested

- Keep a copy for your own records, along with the mailing receipt

- Note the date it was delivered once the receipt comes back

- Avoid sending it by phone or verbally; the FDCPA protection applies to written notice

A cease-and-desist letter doesn't erase the debt, but it legally forces the collector to stop nearly all contact.

What happens after you send it

Once a collector receives your cease-and-desist letter, the law allows them exactly two things: confirm they're stopping contact, or notify you of a specific action they intend to take, like filing a lawsuit. Anything beyond that, including another call to your sister or a follow-up voicemail to your parents, is a direct violation you can act on.

Expect the letter to reduce contact within a week or two in most cases, since agencies track compliance closely to avoid liability. If calls continue anyway, you now have two pieces of documentation working in your favor: the delivery receipt proving they got your notice, and your ongoing log proving they ignored it. Together, those two records make the next step, filing a formal complaint, much stronger than it would be without them.

How to file a complaint against a debt collector

Filing a formal complaint turns your documentation into something that carries consequences for the collector. Regulatory agencies track patterns across companies, and a single complaint from you can join dozens of others already on file against the same agency, which increases the odds of an investigation or fine. This step matters most when a cease-and-desist letter gets ignored, because it shows the collector chose to keep breaking the law even after formal written notice.

Start with the CFPB

Start by filing directly with the Consumer Financial Protection Bureau, the federal agency built specifically to handle disputes like this. Their online portal walks you through uploading your documentation, including your call log and the certified mail receipt from your cease-and-desist letter. The CFPB forwards your complaint to the collector and requires a response within 15 days, and that response becomes part of the public record other consumers can search before dealing with the same company.

A CFPB complaint puts a permanent, searchable mark on a collector's record, and that alone changes how they treat future cases.

Report to your state attorney general and the FTC

Beyond the CFPB, file a second complaint with your state attorney general's office , since Mississippi and Tennessee both investigate consumer protection violations independently of federal action. The Federal Trade Commission also collects debt collection complaints and uses them to build enforcement cases against agencies with repeated violations. Filing in multiple places costs you almost nothing beyond twenty minutes of your time, and it multiplies the pressure on a collector who's betting you won't bother.

What your complaint needs to include

Include specific details every time, since vague complaints get less traction than ones built on hard facts.

- Full name and contact information of the collection agency

- Dates and times of every contact with your family

- What was said, especially any mention of the debt or a demand for payment

- Copies of your cease-and-desist letter and its delivery receipt

- Names of family members contacted, with their permission to reference them

When a complaint isn't enough

Suing a debt collector becomes an option once you can show a clear, documented pattern of violations, and the FDCPA allows you to recover actual damages plus up to $1,000 in statutory damages, along with attorney's fees. Most consumer attorneys take these cases on contingency, meaning you pay nothing upfront, because the law shifts legal costs onto the collector once a violation is proven. If your complaint doesn't stop the calls, or if the harassment already caused real harm to you or your family, a lawsuit is often the fastest way to get both compensation and a permanent end to the contact.

Common scenarios that confuse people

Several situations don't fit neatly into "they called my family" and trip people up when they're trying to figure out if a line got crossed. Below are the ones that generate the most confusion, based on how these disputes actually play out.

Does contacting your spouse count as a family member violation

Spouses occupy a gray area that surprises a lot of people. If you live in a community property state or the debt was jointly held, a collector generally can discuss the account with your spouse because they're considered a co-debtor, not a third party. Tennessee and Mississippi aren't community property states, so unless your spouse's name is actually on the account, they're treated the same as any other relative under the FDCPA. That means the same location-information-only rule applies, and a collector who discusses the debt with a spouse who never signed for it has violated the law just as clearly as if they'd called your sister.

A voicemail left with a relative that mentions the debt

Voicemails create their own trap for collectors, and they often get this wrong. A message left on a family member's phone that references an account number, a balance, or the word "debt" counts as disclosure , even if no human answered the call. Courts have treated these voicemails the same as a live conversation, because the information reaches the third party regardless of format. If a relative plays you a voicemail and you hear any specific reference to money owed, save that recording immediately. It's some of the strongest evidence you can have.

A voicemail that names your debt is just as much a violation as a phone call that does.

When the debt belonged to a deceased relative

Families dealing with a parent's estate face a different but related problem. Collectors sometimes call surviving children or a spouse trying to collect on debt the deceased person owed, implying the family is now responsible. In nearly every case, surviving relatives don't inherit debt personally; it gets paid from the estate, if funds exist, before anything passes to heirs. A collector pressuring you to pay a deceased parent's credit card out of your own pocket is misrepresenting how estate debt actually works.

Calls to your workplace instead of your home

Workplace contact confuses people because it feels different from a family call, but the same rule applies. A collector can call your employer once to confirm you work there or get a number, but they cannot discuss the debt with a receptionist, a supervisor, or a coworker who answers the phone. If your employer's HR department receives a call mentioning collections, that's a violation you can document the same way you would a call to your mother, with the date, time, and exactly what was said.

When it's time to talk to a bankruptcy or consumer attorney

Some situations move past what a letter or a complaint can fix. If a collector kept calling your family after a cease-and-desist letter, disclosed your debt to multiple relatives, or left threatening voicemails, you're no longer dealing with a misunderstanding. You're dealing with a documented FDCPA violation , and a consumer attorney can turn that documentation into real compensation instead of just an apology from a compliance department.

Signs the harassment has crossed into legal territory

Certain patterns tell you it's time to stop handling this alone and bring in a lawyer who handles debt collection cases regularly.

- A relative received calls after you sent a written cease-and-desist letter

- The collector disclosed your balance, account number, or debt status to more than one person

- A family member felt pressured into offering payment

- The calls continued for weeks despite multiple documented requests to stop

- Your CFPB or FTC complaint didn't change the collector's behavior

If a written cease-and-desist letter didn't stop the calls, that alone is grounds for legal action.

Why the underlying debt matters too

Harassment from collectors rarely shows up in isolation. Often it's a symptom of a debt load that's already become unmanageable, which is where a bankruptcy attorney's perspective becomes useful alongside a consumer protection claim. Filing Chapter 7 or Chapter 13 triggers an automatic stay under federal bankruptcy law, and that stay legally stops all collection activity immediately, including calls to family members trying to reach you. For someone drowning in collector contact from multiple accounts, bankruptcy sometimes solves the harassment problem faster than chasing individual FDCPA claims against each agency.

An attorney who handles both bankruptcy and consumer protection cases, which is how Mayfield Law Firm approaches these situations, can look at your full financial picture and tell you honestly which path fixes more of the problem. Sometimes that's a standalone FDCPA lawsuit against the collector. Sometimes it's a bankruptcy filing that ends contact with every creditor at once. Occasionally it's both, since nothing stops you from pursuing damages for past harassment while also filing for the stay that ends future contact.

What to bring to a consultation

Walking in prepared saves time and helps the attorney evaluate your case quickly.

Your contact log (dates, times, what was said)

Copy of your cease-and-desist letter and delivery receipt

Any voicemails saved to your phone or another device

Copies of complaints filed with the CFPB, FTC, or state AG

Basic list of debts, balances, and creditors if bankruptcy is a possibility

Virtually every consumer attorney offers a free initial consultation , so there's no financial risk in finding out where you stand. Bringing organized records means the first meeting focuses on strategy instead of reconstructing what happened, and it gives the attorney what they need to tell you quickly whether you have a strong FDCPA claim, a bankruptcy option worth exploring, or both.

Protecting your family's peace of mind

A debt collector calling family members should never turn into a burden your relatives carry for you. The law draws a clear line: collectors can ask for your location once, and that's it. Everything beyond that, repeated calls, disclosed balances, pressure to pay, is a violation you can document and act on. You now know the steps: gather the facts, send a cease-and-desist letter, file complaints with the CFPB and FTC, and recognize when the harassment has crossed into territory a lawyer needs to handle.

Don't wait for the calls to escalate before you act. Every day you delay gives a collector more room to pressure people you love. If your family has already been contacted, or you're facing debt that feels unmanageable no matter what you do, schedule a free consultation with Mayfield Law Firm and find out exactly where you stand.