Debt Relief Lawyer Near Me: Costs, Options, And Red Flags

When debt starts affecting your sleep, your relationships, and your ability to function day to day, searching for a debt relief lawyer near me feels urgent, and it should. The right attorney can stop creditor harassment, protect your assets, and help you choose a path forward that actually fits your situation. The wrong one can cost you money you don't have and leave you worse off than before.

But here's the problem: not every attorney advertising "debt relief" offers the same services, charges the same fees, or even has your best interests in mind. Some focus on bankruptcy. Others negotiate settlements. A few do both. And scattered among them are outfits that overpromise, underdeliver, and pocket fees before doing any real work. Knowing the difference matters, your financial future depends on it .

At Mayfield Law Firm, P.A., we handle Chapter 7 and Chapter 13 bankruptcy cases for individuals across Northeast Mississippi and South Memphis. We've spent over 40 years helping people navigate financial hardship, and we've seen firsthand what good legal guidance can do, and what happens when people fall for bad advice. This article breaks down what a debt relief lawyer actually does, what you should expect to pay , the options available to you, and the red flags that should make you walk away.

Why hiring a debt relief lawyer can matter

When you're behind on payments, creditors don't wait. Collection calls start immediately , and letters threatening lawsuits or wage garnishment follow shortly after. Most people try to handle this alone by calling creditors directly, negotiating payment plans that become impossible to maintain, or simply ignoring the problem and hoping it resolves itself. That approach rarely works. The moment you involve a licensed debt relief attorney , the dynamic shifts. Creditors must communicate through your lawyer, and the harassment stops by law under the Fair Debt Collection Practices Act.

The legal system is not built for you to navigate alone

Federal bankruptcy law and state-specific exemptions are complicated territory. Missing a single deadline or filing the wrong form can result in your case being dismissed, or losing assets you were legally entitled to protect. A debt relief lawyer near me search might return dozens of results, but what separates a competent attorney from the rest is knowing which legal tools apply to your specific situation and how to deploy them before a creditor moves against you.

Creditors have attorneys working for them. Those attorneys know every legal procedure available to collect what you owe, from wage garnishment to bank levies to property liens. Facing that process alone , without someone who understands those same procedures and how to counter them, puts you at a serious disadvantage from the moment the first collection lawsuit lands in your mailbox.

The moment you file for bankruptcy, federal law triggers an automatic stay that halts most collection actions immediately, giving you time to plan.

What's at stake if you wait

Interest, late fees, and penalty rates compound every month you delay. A $5,000 debt can grow into a garnished paycheck or a frozen bank account faster than most people expect. Every state also has exemption laws that let you protect certain assets in bankruptcy, but you have to claim them correctly and at the right time. Mississippi and Tennessee each have specific rules about what property you can keep, and an attorney who knows those rules can build a strategy around them.

Waiting also narrows your options. Some bankruptcy protections require that you haven't transferred assets or taken on certain types of debt within a specific time window. The longer you delay , the fewer legal tools your attorney has to work with, and the harder it becomes to protect the property and income that matter most to you and your family.

What a debt relief lawyer can do for you

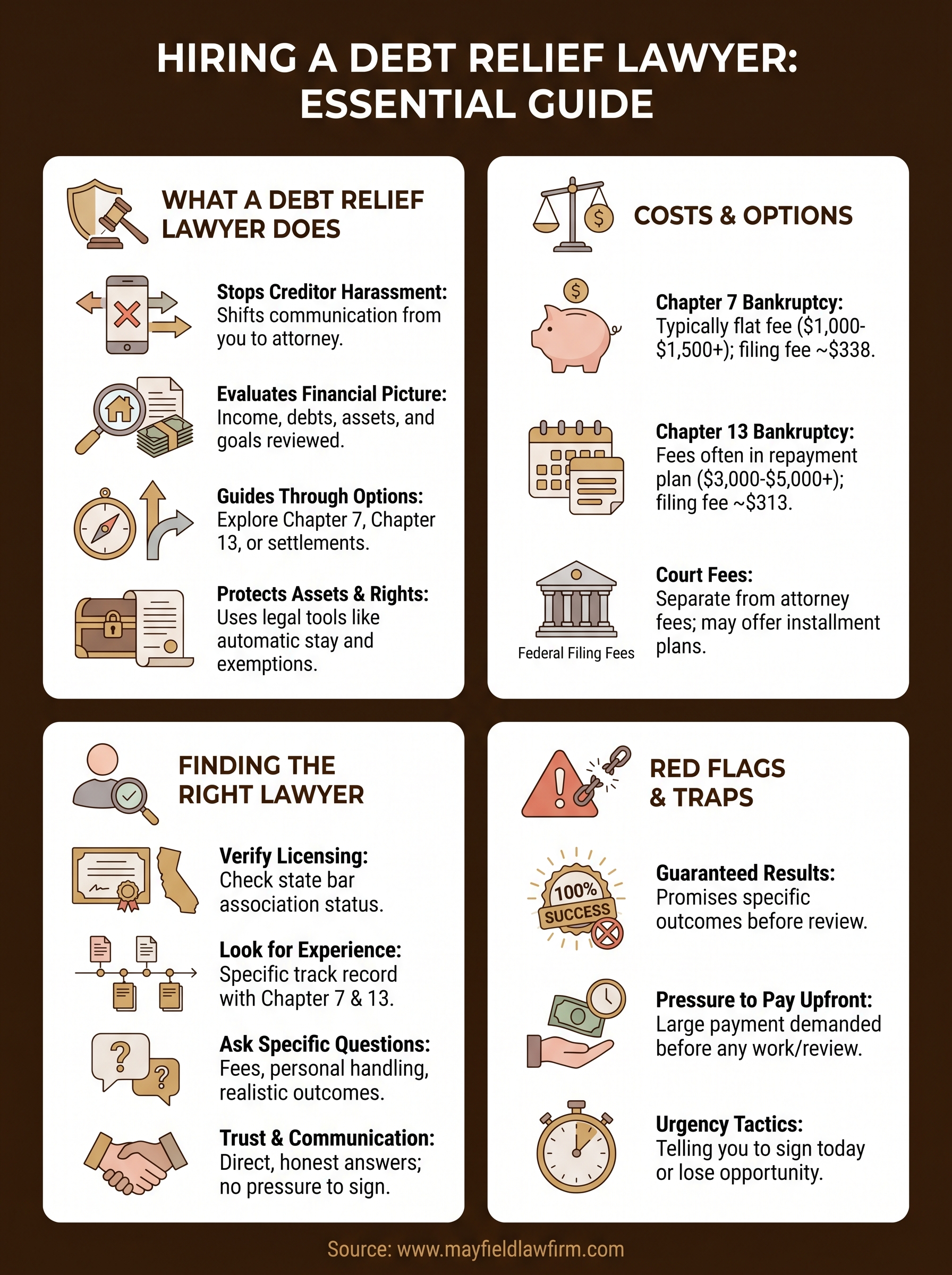

A debt relief lawyer does more than give advice on your options. When you search for a debt relief lawyer near me , you want someone who evaluates your complete financial picture , including your income, your debts, your assets, and your goals, before recommending any course of action. A qualified attorney matches the legal tool to the specific problem rather than applying the same solution to everyone who walks through the door.

Stop creditors in their tracks

Your attorney sends a letter of representation that shifts all collection communication away from you immediately. Creditors and collection agencies must route every call, letter, and legal notice through your lawyer instead of contacting you directly. Your attorney can also take these specific actions on your behalf:

- Challenge invalid or inflated debts

- Dispute inaccurate entries on your credit report

- Push back on any collection activity that violates the Fair Debt Collection Practices Act

Once a bankruptcy petition is filed, the automatic stay goes into effect and legally halts most creditor actions immediately.

Guide you through every legal option

Bankruptcy is not the only path your attorney can explore with you. Chapter 7 bankruptcy can eliminate most unsecured debt within a few months if you qualify, while Chapter 13 bankruptcy lets you restructure what you owe into a manageable repayment plan that runs three to five years.

Your attorney also evaluates whether direct creditor negotiations or debt settlements make more financial sense for your specific situation. A qualified attorney lays out the real consequences of each path , including what happens to your credit, your property, and any co-signers, so you can commit to a plan based on facts rather than fear.

How to find the right debt relief lawyer near you

Running a search for debt relief lawyer near me gives you a list, but that list tells you nothing about whether any of those attorneys are actually qualified to handle your specific type of debt problem. State bar association websites let you verify that an attorney is licensed and in good standing in your state, which should be your first check before scheduling any consultation. A licensed attorney who focuses on debt-related cases brings a different level of practical knowledge than one who occasionally handles a bankruptcy filing between other casework.

Look beyond the website

Every attorney's website presents the best possible version of their practice. What matters more is verifiable experience and a track record with cases like yours. Ask how many bankruptcy cases they have filed, whether they handle both Chapter 7 and Chapter 13, and how familiar they are with state-specific exemption laws in Mississippi or Tennessee. An attorney who handles these cases regularly will answer those questions without hesitation.

Ask the right questions before you sign anything

Before committing to any attorney, bring a list of specific questions to your consultation. A good lawyer gives you direct, honest answers rather than vague reassurances. Consider asking:

- How long have you handled debt relief and bankruptcy cases?

- Will you personally handle my case, or will it go to a paralegal?

- What are all the fees involved , and when are they due?

- What outcome is realistic given my specific financial situation?

A lawyer who promises a specific result before reviewing your documents is one you should walk away from immediately.

Pay attention to how they communicate. If they rush you, dodge specific questions, or pressure you into signing on the spot, those are warning signs worth taking seriously. The attorney-client relationship depends on trust and clear communication , and if that is missing from your very first meeting, it will only get worse once your case is underway.

What it costs to hire a debt relief lawyer

Cost is usually the first concern people raise, and it is a fair one when you are already struggling financially. Chapter 7 bankruptcy attorneys typically charge a flat fee that ranges from around $1,000 to $1,500, though fees vary by location and case complexity. Chapter 13 cases involve more ongoing work and usually cost more, with fees often running between $3,000 and $5,000 spread across your repayment plan.

Court fees and payment options

Beyond attorney fees, federal bankruptcy filing fees add to the total cost. As of 2026, filing for Chapter 7 costs $338 and Chapter 13 costs $313 in federal court. These amounts are separate from what your attorney charges. Many attorneys who handle bankruptcy and debt relief cases allow you to pay fees over time, which makes legal representation more accessible when money is already tight.

If you cannot afford the Chapter 7 filing fee upfront, you can apply directly to the court for a fee waiver or an installment payment arrangement.

What you get for the cost

Hiring a qualified attorney is an investment in protecting your assets, your income, and your legal rights from the moment they take your case. When you search for a debt relief lawyer near me, compare what each attorney includes in their quoted fee, specifically whether they cover creditor correspondence, court appearances, and document preparation. Cheap representation that excludes essential services can end up costing you far more than a higher flat fee that covers everything you need from start to finish.

Debt relief lawyer red flags and common traps

Not every firm that shows up when you search for a debt relief lawyer near me is operating in your best interest. Some outfits charge large upfront fees , disappear once they have your money, and leave you in a worse legal position than when you started. Knowing what to watch for before you hand over a single dollar can protect you from a costly mistake.

Watch out for guaranteed results

No attorney can legally guarantee a specific outcome in any legal matter. If someone promises you a specific result , such as wiping out all your debt or keeping every asset you own, before they have reviewed a single document, that is a serious warning sign. Legitimate attorneys describe realistic possibilities based on your actual financial circumstances, not the best-case scenario designed to get you to sign.

A reputable attorney will tell you what is likely, not what you want to hear.

Pressure to pay before any review

Legitimate debt relief attorneys typically collect fees after reviewing your case and explaining exactly what services those fees cover. Any attorney or company that demands a large payment upfront before doing any work or reviewing your documents is a trap. The Federal Trade Commission has taken action against numerous debt relief companies that collected advance fees and delivered nothing in return.

Urgency tactics are another warning sign. Telling you to sign today or lose the opportunity is a pressure strategy, not a legal reality. Credible legal representation does not come with a countdown clock. Take your time, compare your options, and do not let anyone rush you into a decision before you are ready.

Next steps

You now know what a debt relief lawyer actually does, what it costs, how to find the right one, and which warning signs should make you walk away. The next move is straightforward: gather your financial documents , including your income information, a list of your debts, and any collection notices or lawsuit paperwork you have received, and schedule a consultation with a qualified attorney who handles debt relief cases in your area.

Searching for a debt relief lawyer near me is a starting point, not a solution. The solution comes from sitting down with someone who reviews your specific situation and gives you honest guidance on what your legal options actually are. At Mayfield Law Firm, P.A., we have handled Chapter 7 and Chapter 13 cases across Northeast Mississippi and South Memphis for over 40 years. We offer free consultations , so you can get real answers before committing to anything. Contact our team today and take the first step toward financial stability.