How Does Uninsured Motorist Coverage Work After a Wreck?

You did everything right, carried insurance, followed traffic laws, drove carefully. Then someone without coverage ran a red light and hit you. Now you're stuck with medical bills, a wrecked vehicle, and no way to collect from the at-fault driver. This is exactly the situation that raises the question: how does uninsured motorist coverage work , and will it actually protect you when you need it most? The answer matters more than most drivers realize, especially in Mississippi and Tennessee, where uninsured driver rates remain among the highest in the country .

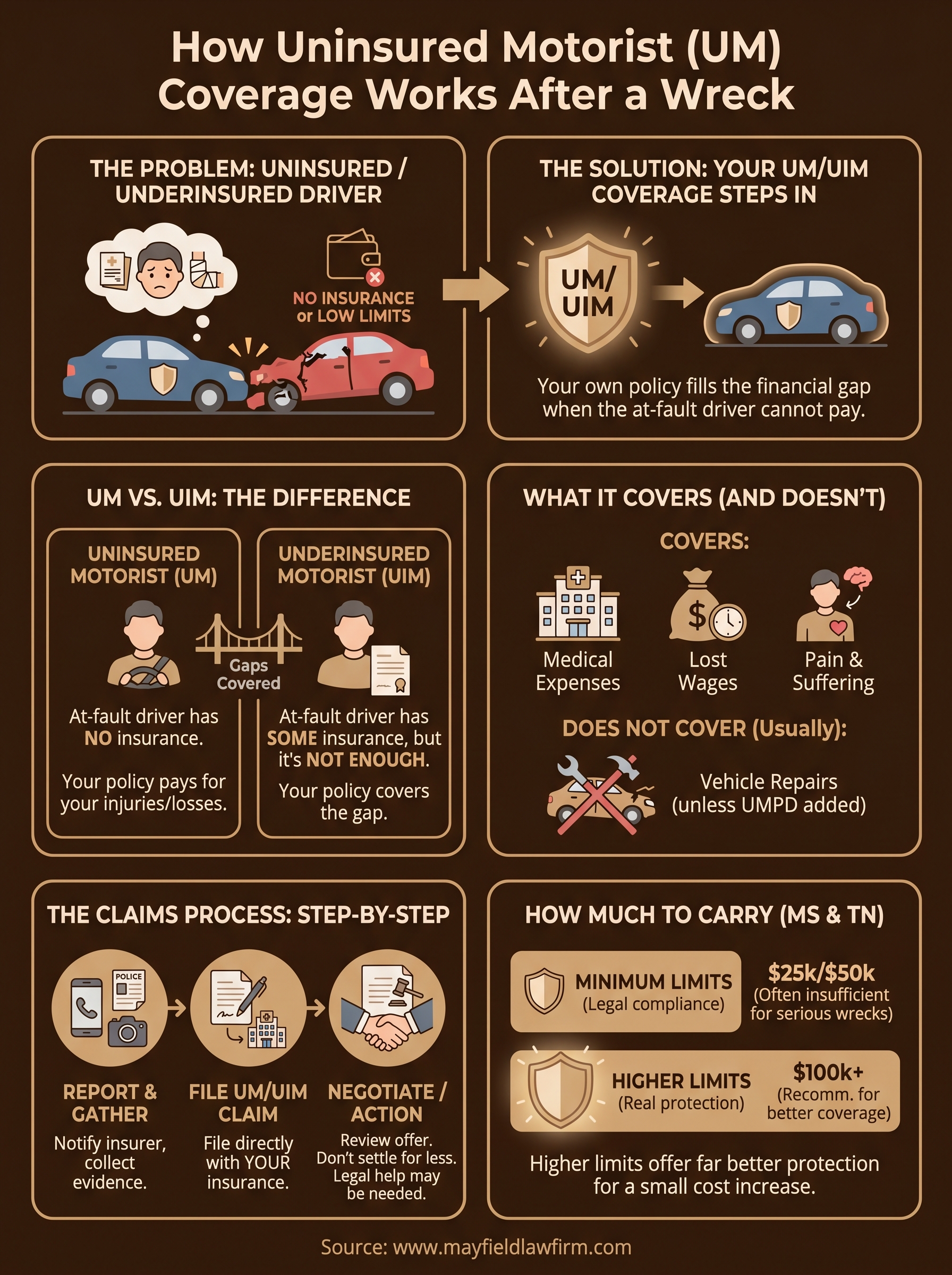

Uninsured motorist (UM) coverage is a provision in your own auto insurance policy that steps in when the other driver has no insurance, or not enough of it. It can cover medical expenses, lost wages, and pain and suffering, depending on your policy. But the claims process isn't always straightforward, and insurance companies don't always make it easy to collect what you're owed, even from your own policy.

At Mayfield Law Firm, P.A., we represent accident victims across Northeast Mississippi and South Memphis who are dealing with exactly these situations. With over 40 years of legal experience handling auto accident and personal injury cases, we've seen how UM/UIM claims play out, and where they go wrong. This article breaks down what uninsured motorist coverage is, how it works after a wreck, and what steps you should take to protect your right to full compensation.

What uninsured motorist coverage is

Uninsured motorist (UM) coverage is a provision in your own auto insurance policy that pays for your injuries and losses when the driver who caused your accident carries no liability insurance at all . Rather than pursuing a driver who has nothing to offer, you file a claim directly with your own insurer. Understanding how does uninsured motorist coverage work comes down to one core idea: your policy fills the gap left by an at-fault driver who cannot pay.

In Mississippi and Tennessee, where uninsured driver rates consistently rank among the highest in the country, this coverage is one of the most important protections you can carry.

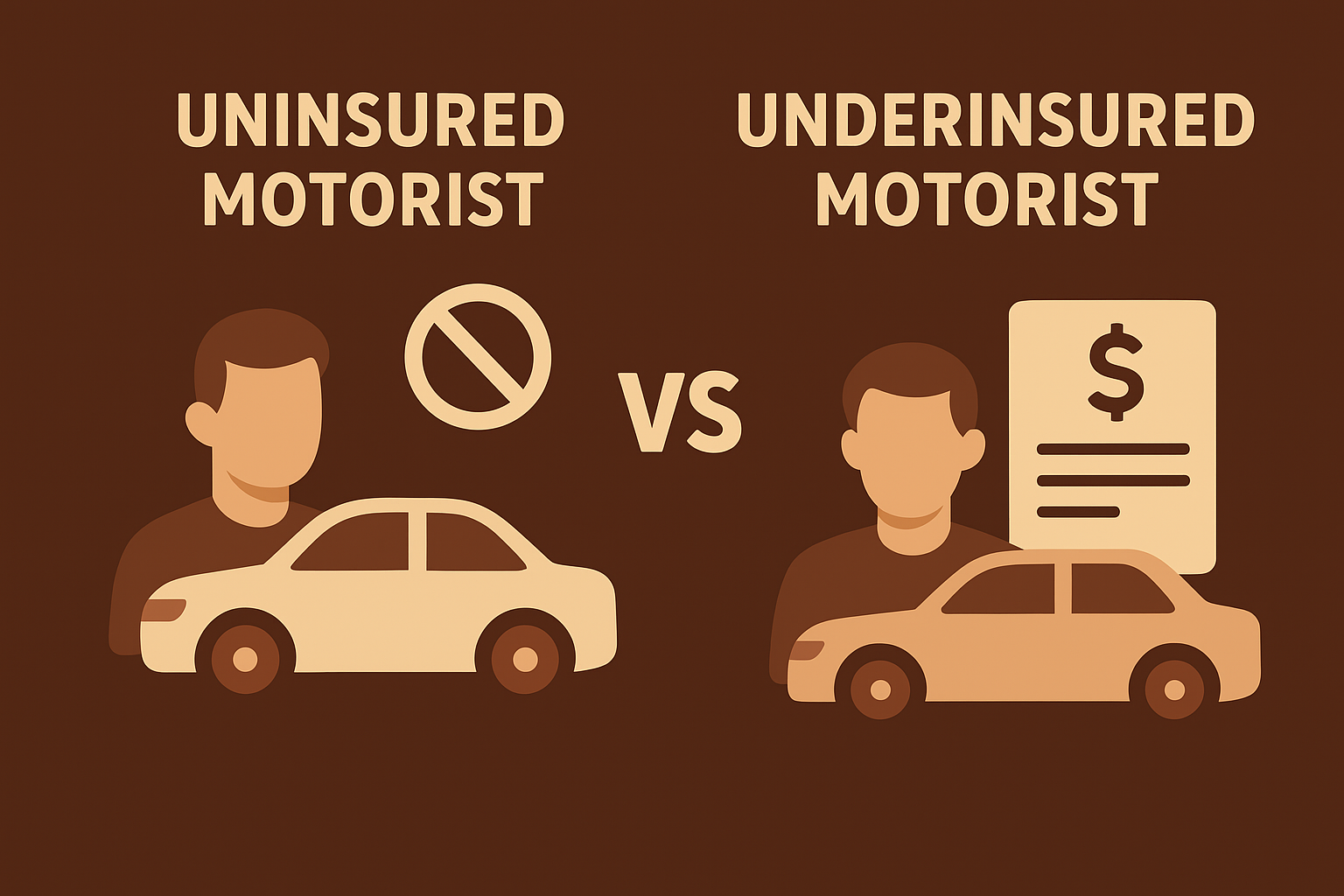

The difference between UM and UIM

UM and UIM are related but serve different situations, and the distinction matters when you're recovering from a wreck. Uninsured motorist (UM) coverage applies when the at-fault driver carries absolutely no insurance policy of any kind. Your own policy becomes the only available source of compensation for your injuries and losses.

Underinsured motorist (UIM) coverage applies when the at-fault driver has insurance, but their policy limits fall short of your actual damages. For example, if the other driver carries $25,000 in liability coverage but your medical bills total $80,000, your UIM policy can cover the remaining gap up to your own selected limits.

How UM and UIM fit into your policy

Both coverages typically appear together as a single line item on your policy's declarations page. Mississippi law requires insurers to offer UM coverage , though drivers may reject it in writing. Tennessee follows a similar structure, with insurers required to offer UM/UIM limits that match your liability limits. You can choose a lower amount, but doing so directly reduces your protection in a serious accident. Reviewing your current policy limits before a wreck happens puts you in a much stronger position when it's time to make a claim.

What UM and UIM cover and what they do not

Understanding what your UM/UIM policy actually pays for is essential before you file a claim. Coverage varies by policy and state, but most standard provisions follow a clear pattern when you consider how does uninsured motorist coverage work in practice.

What these coverages pay for

UM and UIM coverage typically pays for medical expenses , including emergency care, surgery, and ongoing rehabilitation costs. Your policy can also cover lost wages during recovery, pain and suffering, and wrongful death damages for surviving family members in fatal crashes.

Key costs UM/UIM commonly covers:

- Emergency room and hospital bills

- Ongoing treatment and physical therapy

- Lost income while you're unable to work

- Pain and suffering damages

In Mississippi and Tennessee, UM coverage also applies to hit-and-run accidents, treating them the same as uninsured driver scenarios under most standard policy terms.

What these coverages do not pay for

Most UM/UIM policies do not cover vehicle repair or replacement unless you carry uninsured motorist property damage (UMPD) as a separate add-on to your policy. Your coverage also will not pay beyond your selected policy limits , regardless of how large your actual medical bills and losses turn out to be.

Why UM and UIM matter after a wreck

Mississippi and Tennessee both rank among the states with the highest rates of uninsured drivers in the country. Without UM/UIM coverage, your only option after a wreck caused by an uninsured driver is to sue that person directly, which often produces nothing when the at-fault driver has no assets or income to collect from.

A court judgment against an uninsured driver is only worth something if that driver actually has money or property to pay it.

The real cost of going without this coverage

Medical bills after a serious accident climb fast. Emergency care, surgery, and physical therapy can total tens of thousands of dollars within weeks of a wreck. If the at-fault driver carries no insurance, you absorb every dollar of that cost out of pocket unless your UM policy steps in to cover it.

Lost income compounds the financial damage. Missing weeks or months of work during recovery adds pressure on top of existing medical debt, often pushing families toward bankruptcy. Knowing how does uninsured motorist coverage work gives you a clearer picture of why carrying adequate UM/UIM limits is one of the most practical decisions you can make before you ever need to file a claim.

How a UM or UIM claim works step by step

Once you understand how does uninsured motorist coverage work in theory, the actual claims process becomes the next critical piece. Filing with your own insurer after someone else caused your accident feels counterintuitive, but the steps are manageable when you know what to expect ahead of time.

Report the accident and gather evidence

Notify your insurance company as soon as possible after the wreck. Collect the police report, photographs of the scene , and any witness contact information before you leave. Your insurer will ask for all of it when they open your file.

File your UM or UIM claim

Contact your insurer directly and open a formal UM or UIM claim . Submit your documentation, medical records, and proof of lost wages along with the claim. An adjuster will be assigned to evaluate your total losses and determine a settlement value.

Insurance companies sometimes dispute UM/UIM claims or offer settlements far below your actual damages, even when you are their own policyholder.

Negotiate or pursue legal action

Your insurer will present a settlement offer based on their adjuster's assessment. If that figure does not cover your actual medical bills and lost income , you have the right to negotiate or file a lawsuit against your own insurer to recover what you are owed.

How much coverage to carry in Mississippi and Tennessee

Mississippi's minimum UM coverage requirement mirrors the state's liability minimums: $25,000 per person and $50,000 per accident. Tennessee follows the same structure, with minimum UM/UIM limits starting at $25,000 per person and $50,000 per accident. Those floors meet the legal threshold, but they rarely cover the full cost of a serious wreck with meaningful medical treatment or lost income.

Minimum limits give you legal compliance, not real protection when your actual damages climb past those caps.

Why higher limits protect you better

Understanding how does uninsured motorist coverage work at higher limits makes a direct difference in your recovery. Medical bills from a single hospitalization can easily reach $75,000 or more , leaving you responsible for every dollar above your policy cap. Carrying $100,000 per person or higher gives you meaningful protection when the at-fault driver has nothing to offer.

Both Mississippi and Tennessee allow you to select higher UM/UIM limits than the state minimum, and that upgrade typically costs far less than most drivers expect.

What to review on your current policy

Check your declarations page to confirm your UM/UIM limits before a wreck happens. Ask your insurer whether UMPD coverage is available as a separate add-on, since standard UM policies typically exclude vehicle repair costs entirely.

Quick recap and when to get legal help

UM/UIM coverage fills the gap when the at-fault driver carries no insurance or not enough coverage to pay your full damages. Knowing how does uninsured motorist coverage work gives you a real advantage before and after a wreck. It covers medical bills, lost wages, and pain and suffering, but not vehicle repairs unless you carry UMPD as a separate add-on. Mississippi and Tennessee both require insurers to offer it, and carrying higher than minimum limits puts you in a far stronger position when your actual costs exceed those state-set floors.

Filing a UM or UIM claim against your own insurer can get complicated fast. Adjusters often undervalue claims , and low settlement offers are common even when your losses are well-documented. If you've been in a wreck involving an uninsured or underinsured driver, contact Mayfield Law Firm, P.A. for a free consultation and get experienced representation working for you.