How Much Can Be Garnished from Your Paycheck?

When a creditor starts taking money straight out of your paycheck, you need to know exactly how much can be garnished from paycheck amounts before you panic or make a decision you'll regret. Federal law caps most creditor garnishments at 25% of your disposable earnings, but that number shifts depending on who's collecting and what you owe. Child support, student loans, and tax debt each follow their own rules, and Mississippi and Tennessee add their own wrinkles on top of the federal floor.

The short answer: it depends on the debt type, but there are hard limits nobody can cross, and knowing them tells you immediately whether your employer is taking too much. We'll walk through the federal garnishment limits set by the Consumer Credit Protection Act, then break down how child support and student loan garnishments work differently from ordinary credit card or medical debt.

We'll also cover what protections apply if you're already living paycheck to paycheck, and when bankruptcy can stop the garnishment altogether. If you're facing wage garnishment in Southaven or Memphis, this is the information you need before your next payday.

Why paycheck garnishment limits matter to you

Garnishment limits exist because Congress recognized a simple fact: a worker stripped of too much income can't pay rent, buy groceries, or keep a car running to get to the job that generates the paycheck in the first place. The Consumer Credit Protection Act set a ceiling on creditor garnishments back in 1968, and that ceiling still protects you today. Without it, a single unpaid medical bill or credit card default could theoretically wipe out your entire check, pushing you into a spiral that costs you your housing or your job.

Knowing your rights here isn't just legal trivia. If your employer's payroll department miscalculates a garnishment order, or a creditor's attorney pushes for more than the law allows, you're the one who feels it in your bank account. Employers process garnishment orders every week, and mistakes happen more often than you'd think, especially when a worker has multiple garnishments running at once or an unusual pay schedule. Catching an error early can mean the difference between covering your utility bill and facing a shutoff notice.

Federal law puts a hard ceiling on wage garnishment specifically so a paycheck can never be reduced below what a person needs to survive.

Understanding these limits also shapes your next move. If you're already at the legal maximum, you know you can't be squeezed further by that same creditor, though a second creditor with a different type of debt can sometimes still take a cut. If you're facing multiple garnishments for child support, taxes, and consumer debt simultaneously, the combined limits matter even more, because federal and state caps interact in ways that surprise most people. That's exactly the kind of situation where a quick conversation with a bankruptcy attorney can clarify whether relief is available before your finances collapse under the weight of competing collection orders.

Federal limits on wage garnishment by debt type

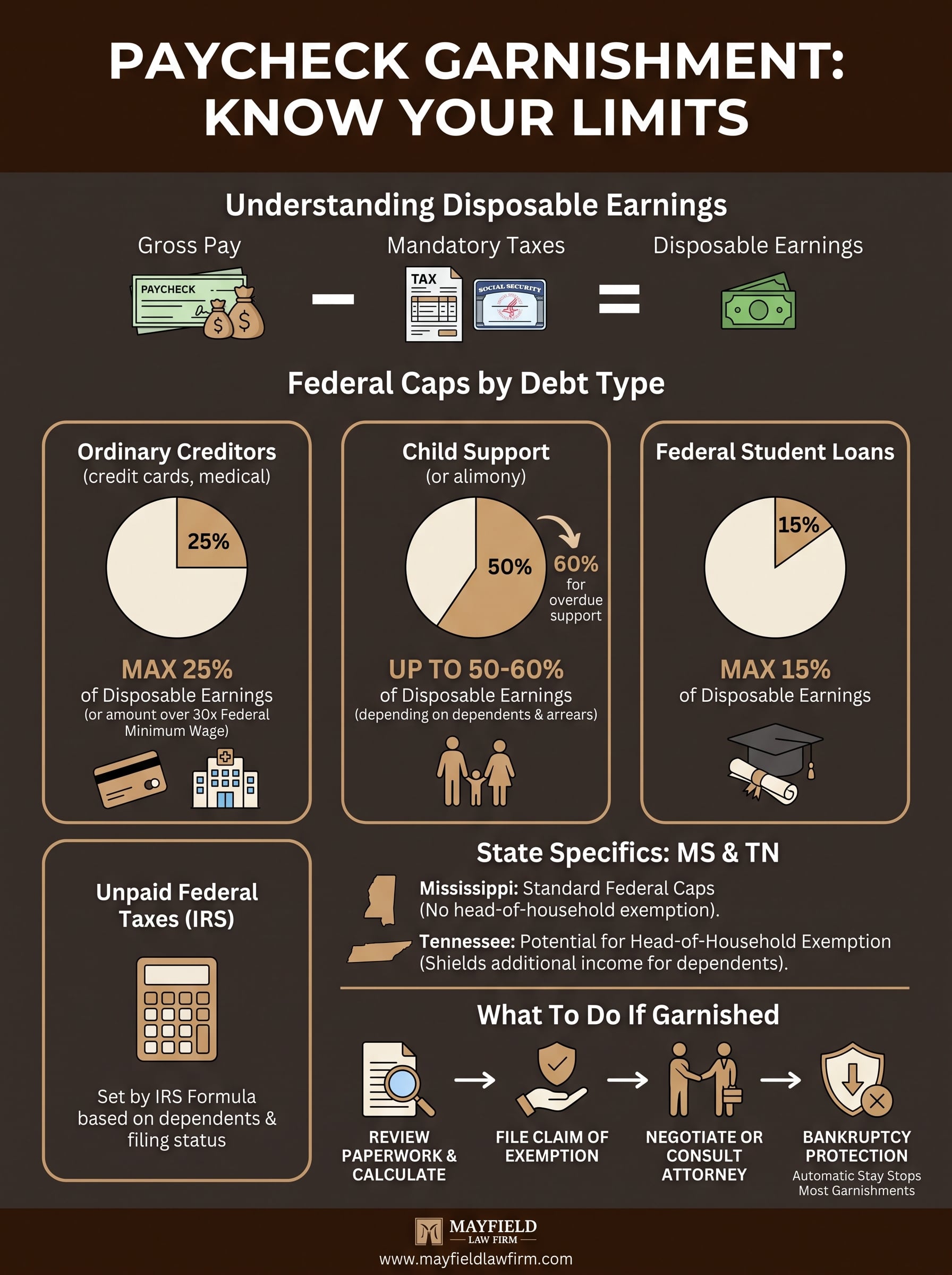

The Consumer Credit Protection Act sets the outer boundary for every garnishment order, but the actual cap swings widely depending on who's collecting. Ordinary creditors, like credit card companies or medical debt collectors, can only take the lesser of 25% of your disposable earnings or the amount by which your weekly pay exceeds 30 times the federal minimum wage. Child support, taxes, and student loans play by different rules entirely.

No matter the debt, federal law never lets a single garnishment order swallow your entire paycheck.

Comparing the caps by debt type

This table shows how differently the government treats each category:

| Debt Type | Federal Maximum Garnishment |

|---|---|

| Credit card, medical, personal loans | 25% of disposable earnings |

| Child support (no other dependents) | Up to 60% of disposable earnings |

| Child support (supporting another child/spouse) | Up to 50% of disposable earnings |

| Federal student loans | 15% of disposable earnings |

| Unpaid federal taxes (IRS) | Set by IRS formula based on dependents |

Why the gaps exist

Congress built in higher limits for child support enforcement because courts treat supporting a child as a higher priority than repaying a credit card. Add a 5% bump if you're more than 12 weeks behind on support payments. The U.S. Department of Labor publishes the full breakdown if you want to check your specific situation.

How state law can lower your garnishment amount

Federal law sets the ceiling, but Mississippi and Tennessee can only push that number down, never up. States are free to protect more of your paycheck than the federal minimum requires, and both states in Mayfield Law Firm's service area have done exactly that in certain situations. Neither state currently caps ordinary creditor garnishment below the federal 25% threshold, but the details around exemptions and head-of-household status still shift what actually leaves your check.

Mississippi and Tennessee specifics

Tennessee offers an extra layer of protection: if you support a spouse or minor children, you can claim a head-of-household exemption that shields additional income beyond the federal floor. Mississippi doesn't offer that same exemption, so residents there typically see the standard federal cap apply without additional state-level relief.

Never assume the federal 25% is your final number. Your state's exemptions might legally protect more of your paycheck.

Understanding which rules govern your case matters because a garnishment calculated under the wrong standard can cost you real money every pay period. Verifying your state's specific protections, or having an attorney verify them for you, catches errors before they drain your account for months.

How to calculate your disposable earnings and garnishment

Disposable earnings aren't your gross pay. They're what's left after your employer subtracts legally required deductions like federal income tax, Social Security, and Medicare. Health insurance premiums, retirement contributions, and voluntary deductions don't count against this figure, which surprises a lot of people who assume their take-home pay is the starting point for how much can be garnished from paycheck calculations.

Running the numbers yourself

Grab your pay stub and work through these steps:

- Start with gross wages for the pay period.

- Subtract mandatory tax withholdings only.

- That result is your disposable earnings.

- Multiply by 25% (or the applicable percentage for your debt type).

- Compare that figure to 30 times the federal minimum wage subtracted from weekly disposable earnings.

- The garnishment amount is whichever number is smaller.

Your disposable earnings, not your take-home pay, are the number every garnishment calculation actually depends on.

Most payroll software runs this automatically, but automated systems still make mistakes, especially with irregular overtime or bonus pay. Recalculating it yourself once, using your actual pay stub, tells you immediately whether your employer's garnishment matches what federal and state law actually allow.

How to respond if your paycheck is being garnished

Getting a garnishment notice doesn't mean you're powerless. You have specific windows to act, and missing them costs you options that could have protected your income.

Steps to take right away

Review the paperwork the moment it arrives. Check the math against what you learned above, verify the debt is actually yours, and confirm nobody skipped a required court step before the order landed on your employer's desk.

- Request an itemized breakdown from your employer's payroll department

- File a claim of exemption if the garnishment exceeds legal limits or threatens essential income

- Contact the creditor's attorney to negotiate a lower voluntary payment instead

- Talk to a bankruptcy attorney if multiple garnishments are stacking up

A garnishment order isn't the end of the conversation. It's the start of a deadline you need to act on fast.

When bankruptcy stops the bleeding

Filing Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay that halts most wage garnishments immediately, often within days. This doesn't work for every debt type. Child support obligations survive bankruptcy, and some tax garnishments continue depending on the circumstances. Still, for consumer debt drowning your paycheck, bankruptcy protection often delivers faster relief than negotiating with creditors directly.

Protecting your paycheck going forward

Knowing how much can be garnished from paycheck rules allow is the first step toward keeping more of what you earn. Federal caps set the outer limit, state exemptions sometimes push that number down further, and the math behind disposable earnings determines what actually lands in your account each payday. None of that knowledge helps you, though, if you never check your pay stub against the numbers you learned here.

Running your own calculation catches employer errors before they cost you months of overpayment. Filing a claim of exemption stops an illegal garnishment in its tracks. And when multiple creditors are pulling from the same paycheck, bankruptcy protection can halt the bleeding faster than negotiating alone.

If garnishment is already squeezing your budget in Southaven or Memphis, don't wait until the next payday to act. Schedule a free consultation with Mayfield Law Firm and find out exactly what options are available to protect your income.