Can You Sue An Uninsured Driver? Options If They Can't Pay

You just got hit by someone with no insurance. Your car is damaged, you're hurt, and now you're wondering, can you sue an uninsured driver ? The short answer is yes. You absolutely have the legal right to file a lawsuit. But the harder question is whether you'll actually collect any money from someone who couldn't even afford liability coverage.

This is a situation we see regularly at Mayfield Law Firm, P.A., working with injured clients across Northeast Mississippi and South Memphis . An uninsured driver causes a wreck, and suddenly the person who did nothing wrong is stuck figuring out how to pay their own medical bills . It's frustrating, and the legal path forward isn't always obvious.

This article breaks down your options, from filing a lawsuit against the at-fault driver to tapping into your own insurance coverage , so you can make an informed decision about the best way to pursue the compensation you're owed .

Why uninsured driver cases feel different

When a standard car accident happens, the process follows a familiar path. You file a claim with the at-fault driver's insurer, they investigate, and you negotiate a settlement. That system works because liability insurance is required by law in most states, including Mississippi. When the other driver has no coverage, that entire system collapses, and you're suddenly left covering losses caused by someone else's negligence.

The insurance buffer is gone

In a normal claim, you deal with an insurance company , not the at-fault driver personally. The insurer carries a contractual obligation to pay valid claims, so there's an entity with actual money on the other side of the table. Without insurance, you're dealing directly with the individual who hit you, and that shift makes everything harder and more uncertain.

When there's no insurance policy in place, the money has to come from the driver's personal assets, your own coverage, or both.

The "judgment proof" problem

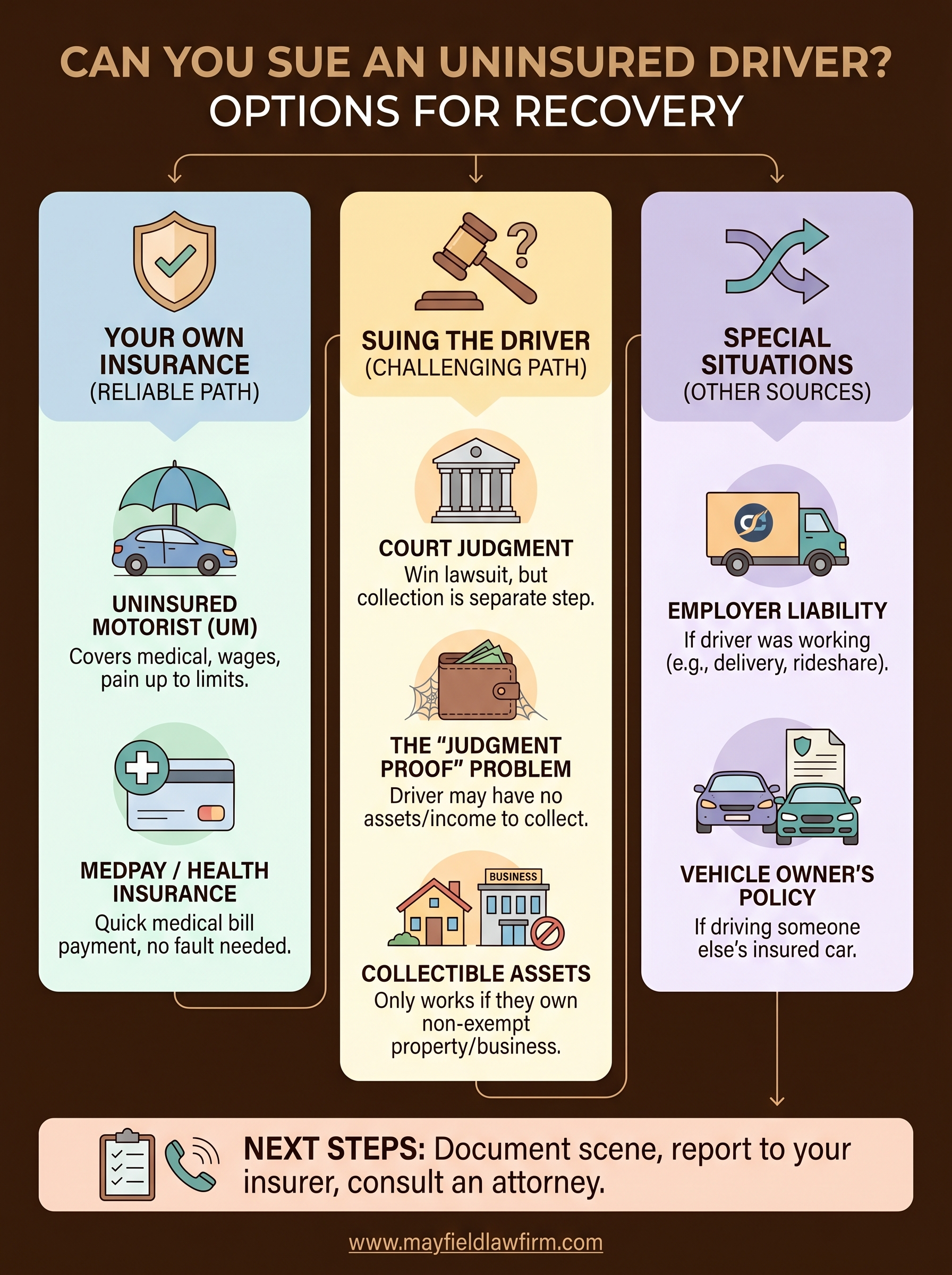

Even if you win a lawsuit against an uninsured driver, collecting that money is a separate challenge entirely. A court judgment says the driver owes you a specific amount, but if that person has no meaningful income or assets , enforcing the judgment becomes nearly impossible. Lawyers call this being "judgment proof." You can absolutely sue an uninsured driver, but whether you'll ever see payment depends entirely on what they actually own.

Some assets are protected from collection even after you win in court, including certain retirement accounts and homestead property under Mississippi law. Knowing what the driver owns before filing a lawsuit helps you decide whether litigation is worth your time and legal costs.

Mississippi's uninsured driver numbers

Mississippi consistently ranks among the states with the highest rates of uninsured drivers in the country. Roughly one in four Mississippi drivers carries no liability insurance at all, which means your odds of being hit by an uninsured driver here are well above the national average . This reality is exactly why experienced attorneys look beyond a simple lawsuit when building a recovery strategy for their clients, and why understanding every available option matters from the moment the crash happens.

Can you sue an uninsured driver and win in court

Yes, you can sue an uninsured driver in civil court, and winning a judgment is entirely possible. The legal process works the same way it would against any other at-fault driver. You file a complaint, gather evidence, and if the facts support your case, a judge or jury will rule in your favor. The real distinction is not whether you can win. It's whether you can actually collect the money the court awards you.

What the court process looks like

Filing a lawsuit starts with proving fault and damages . You'll need to show the other driver acted negligently, caused the crash, and that you suffered real losses as a result. Mississippi uses a pure comparative fault system , so your recovery may decrease if you share any portion of blame, but you still retain the right to pursue the at-fault party. Key losses you can claim include:

- Medical bills and future treatment costs

- Lost wages and reduced earning capacity

- Pain, suffering, and emotional distress

- Property damage

Winning the lawsuit and collecting the money are two completely separate events, and you need a strategy for both.

What happens after you win

Once a court enters a judgment in your favor , you gain legal tools to pursue collection, including wage garnishment, bank account levies, and liens against property. These tools only produce results when the driver has actual income or assets worth pursuing. If they own nothing of value, the judgment may sit dormant until their financial situation changes, which is exactly why evaluating the driver's finances before you file is a critical first step.

How to get paid without suing the driver

Suing an uninsured driver is one option, but your own insurance policy may offer a faster and more reliable path to compensation. Before you decide to pursue the at-fault driver in court, check what coverage you already carry , because in many cases your policy becomes the primary tool for recovering what you lost.

Uninsured motorist coverage

Uninsured motorist (UM) coverage is specifically designed for situations like this. When the at-fault driver carries no liability insurance, your own UM policy steps in and covers your losses up to your policy limits. Mississippi law requires insurers to offer UM coverage, though drivers can reject it in writing. If you accepted UM coverage when you bought your policy, this is often your strongest option for recovering damages without the uncertainty of chasing an individual defendant.

Your UM coverage handles the same types of losses a liability claim would, including medical expenses, lost wages, and pain and suffering.

Checking your policy declarations page confirms whether UM coverage is active and shows your exact limits. If your limits fall short of your actual losses, an attorney can quickly identify whether additional recovery options apply to your situation.

MedPay and health insurance

Medical payments coverage (MedPay) is another policy provision that pays your medical bills regardless of who caused the crash. It works quickly and doesn't require proving fault first. If you don't carry MedPay, your health insurance can cover treatment costs while you pursue other claims. Neither option compensates you for pain and suffering or lost wages, but both keep medical bills from piling up while your case moves forward.

When suing an uninsured driver makes sense

Suing an uninsured driver is not always a waste of time. If the at-fault driver has real assets or a steady income , a court judgment gives you legal tools to pursue collection that actually produce results. The key is doing your homework before you file, so you're not spending money on litigation against someone who has nothing for you to collect.

Signs the driver has collectible assets

You can sue an uninsured driver and come out ahead when the defendant owns property, vehicles, or a business that fall outside protected exemptions. In Mississippi, certain assets like non-homestead real estate and non-exempt personal property can be reached through a judgment lien or levy. If a background check or public records search reveals the driver owns real property or runs a business, litigation becomes a much more practical choice.

A judgment lien attached to the driver's property means you get paid when they sell or refinance, even years down the road.

When the damages are large enough to justify litigation

Litigation carries real costs , including court fees, discovery expenses, and attorney time. For smaller claims, those costs may outweigh what you're likely to recover. However, when your losses involve serious injuries, ongoing medical care, or significant lost wages , the potential recovery justifies pursuing the driver directly in court. Your attorney can run the numbers and compare the expected recovery against the cost of litigation before you commit to filing. That analysis is a practical step you should take before making any final decision.

Special situations that change your options

Not every uninsured driver accident follows the same script. Certain facts about how the crash happened or who the driver was working for can open up additional compensation sources beyond suing the driver personally. Before you assume you're stuck chasing someone with no money, take time to examine every detail of the situation, because those details can change your options significantly.

The at-fault driver was on the job

If the uninsured driver was working at the time of the crash, their employer may carry liability coverage that applies directly to your losses. Employers are generally responsible for accidents caused by employees who were acting within the scope of their work duties at the time. Workers who commonly fall into this category include:

- Delivery drivers completing business runs

- Rideshare drivers on an active fare or trip

- Employees running company errands

Commercial liability policies held by employers tend to carry much higher limits than personal auto coverage, which makes this a valuable avenue when it applies.

When the driver was acting within the scope of employment, the employer's commercial policy becomes a legitimate and significant recovery target.

The driver was operating someone else's vehicle

When a driver borrows another person's car with no insurance of their own , the vehicle owner's liability policy often responds first. Insurance typically follows the car, not the driver, so the owner's coverage may pay your damages up to its limits.

If those limits fall short of your actual losses, you can still ask whether you can sue an uninsured driver for the remaining balance. Confirming vehicle ownership at the scene and documenting that information in your accident report protects this avenue before key details disappear.

Next steps after an uninsured driver crash

After a crash with an uninsured driver, the actions you take in the first days matter more than most people realize. Document everything at the scene , including photos of damage, the other driver's license and registration, witness contact information, and any visible injuries. Report the crash to your own insurer immediately , even if you plan to sue the at-fault driver, because delay can limit your coverage options under your uninsured motorist policy.

Whether you can you sue an uninsured driver and actually recover money depends heavily on the specific facts of your situation, including the driver's assets, your coverage, and whether third parties like employers share responsibility. Every case is different, and making the wrong move early can cost you real money. The team at Mayfield Law Firm, P.A. has handled these cases for decades and knows how to build a recovery strategy that works. Contact our personal injury attorneys today for a free consultation.