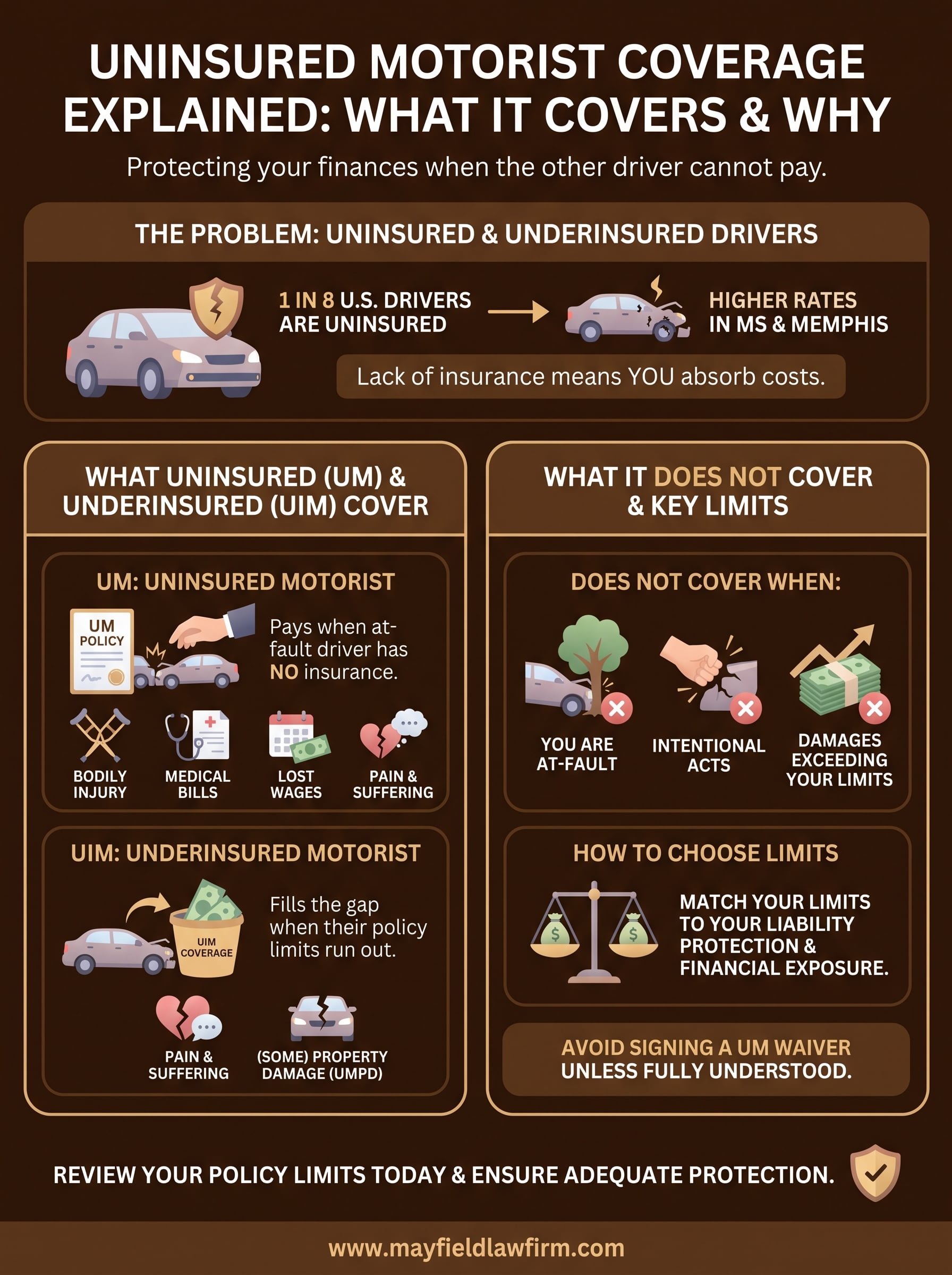

Uninsured Motorist Coverage Explained: What It Covers & Why

Getting hit by a driver who has no insurance, or not enough of it, is more common than most people think. About one in eight drivers on the road carries no auto insurance at all, and that number climbs even higher in states like Mississippi. If you're searching for uninsured motorist coverage explained , chances are you either want to understand what you're paying for or you're trying to figure out how to protect yourself before it's too late.

Uninsured motorist (UM) coverage is the part of your own auto insurance policy that steps in when the other driver can't pay for the harm they caused. It covers medical bills, lost wages, and other damages that would otherwise come straight out of your pocket. Without it, you could win every argument about who was at fault and still walk away with nothing , simply because the at-fault driver had no policy to claim against. That's a situation our attorneys at Mayfield Law Firm, P.A. see regularly when representing accident victims across Northeast Mississippi and South Memphis.

This article breaks down what uninsured and underinsured motorist coverage actually includes, how it works when you need to file a claim, and whether carrying it makes sense for your situation. Understanding these details now can save you from a painful financial surprise later.

Why UM and UIM matter for drivers in the real world

Part of getting uninsured motorist coverage explained correctly means understanding how often this situation actually comes up on real roads. According to the Insurance Research Council , roughly 12.6% of U.S. drivers carry no auto insurance at all. Mississippi's rate sits nearly three times higher than the national figure, consistently placing it among the states with the largest share of uninsured drivers in the country.

In Mississippi, close to one in three drivers may be on the road with no active auto insurance policy.

When the at-fault driver has no insurance

If an uninsured driver causes your crash, you have no third-party policy to file a claim against . Taking that driver to court is an option, but most people who skip insurance do so because they simply cannot pay a judgment even if you win. That leaves you absorbing costs that should never have been yours. Without UM coverage on your own policy, those out-of-pocket losses typically include:

- Medical treatment and hospital bills

- Lost wages while you recover

- Property damage to your vehicle

When the at-fault driver carries minimum limits

Mississippi law sets its minimum bodily injury liability requirement at just $25,000 per person. A serious crash involving surgery, follow-up care, or weeks away from work can produce medical and wage loss totals that far exceed that cap. Once the at-fault driver's policy pays out, you absorb every dollar above the limit .

Underinsured motorist coverage closes the distance between what the other driver's policy pays and what your actual damages total. Without it, you are left negotiating medical debt and lost income with no additional source of recovery, no matter how clearly the other driver caused the crash.

What uninsured and underinsured coverage means

These two coverages are related but they address different problems. Uninsured motorist (UM) coverage pays when the at-fault driver carries absolutely no liability insurance. Underinsured motorist (UIM) coverage pays when the at-fault driver has insurance but not enough to cover your full losses. Many insurers bundle them together, but understanding each one separately helps you make a smarter purchasing decision.

Uninsured motorist (UM) coverage

UM coverage activates when you can show that another driver caused your injuries and that driver carried no active auto insurance policy at the time of the crash. Your own insurer steps in as the payer. This is the core of what most people mean when they search for uninsured motorist coverage explained: your policy fills the gap left by a driver who broke the law by driving without coverage.

Underinsured motorist (UIM) coverage

UIM coverage applies when the at-fault driver had insurance but their policy limits run out before your damages are fully paid. You collect from their policy first, then turn to your UIM coverage for the remainder.

Carrying both UM and UIM together gives you the most complete protection against gaps in another driver's coverage.

What UM and UIM cover and what they do not

When getting uninsured motorist coverage explained in full, the coverage boundaries matter as much as the benefits. Both UM and UIM generally pay bodily injury damages , including medical bills, lost wages, pain and suffering, and wrongful death expenses. Some policies also extend to uninsured motorist property damage (UMPD) , which covers vehicle repairs when the at-fault driver carries no coverage at all.

What these coverages typically include

Both UM and UIM policies pay for bodily injury losses that stem directly from the crash. Coverage typically includes medical treatment and rehabilitation , lost wages during recovery, pain and suffering, and wrongful death expenses for surviving family members.

Selecting higher UM and UIM limits costs relatively little extra on most policies but can protect you against tens of thousands in uncovered losses.

- Medical treatment, surgery, and follow-up care

- Lost income while you recover

- Pain and suffering damages

- Wrongful death and funeral expenses

What UM and UIM do not cover

UM and UIM do not apply when you caused the accident . These coverages also stop at your own selected policy limits , leaving you exposed if your injuries push damages above that ceiling.

Common exclusions include:

- Accidents where you are the at-fault driver

- Damages that exceed your chosen coverage limits

- Intentional acts

- Business use of a personal vehicle without a commercial endorsement

How uninsured motorist claims work after a crash

After a crash with an uninsured or underinsured driver, your own insurer becomes the party you file against. The process follows similar steps to any auto insurance claim, but a few key differences apply because you are dealing with your own policy rather than the other driver's carrier.

Filing promptly and documenting everything from the start gives your claim the strongest possible foundation.

Steps to take immediately after the accident

Calling the police and getting an official crash report is the first step you should take. That report establishes fault on record and documents that the other driver had no valid insurance . Collect the other driver's name, license number, and any insurance information they carry, even if it turns out to be expired or invalid.

- Take photos of vehicle damage, injuries, and the scene

- Get witness contact information before leaving

- Notify your own insurer as soon as possible

What your insurer does with the claim

Your insurance company will investigate the claim, review medical records and wage loss documentation , and determine what your policy limits cover. Part of getting uninsured motorist coverage explained properly is knowing that your insurer may still dispute the value of your damages.

If negotiations stall, an experienced attorney can help you push back and recover the full amount your policy allows. Insurers sometimes undervalue UM claims, treating them the same way they handle third-party claims they want to settle quickly and cheaply.

How to choose limits and avoid common mistakes

Choosing the right UM and UIM limits is where uninsured motorist coverage explained in theory often fails to translate into action. Most drivers accept default limits their insurer offers, which typically mirror the state's bare minimum liability requirements and leave a significant gap when serious injuries occur.

Your UM and UIM limits should be at least as high as your own liability limits to avoid absorbing costs that the other driver caused.

Match your limits to your actual financial exposure

Setting higher coverage limits costs far less than most drivers expect. Bumping bodily injury UM coverage from $25,000 to $100,000 typically adds only a small amount to your monthly premium while protecting you against catastrophic medical and wage loss expenses that a minimum policy would never cover.

Consider your household income and monthly obligations , along with the medical costs typical for serious injuries in your area. A limit that looks adequate today may fall short after a hospital stay, surgery, and several weeks away from work.

Mistakes that leave you underprotected

Signing a UM coverage waiver without reading it carefully is one of the most common errors drivers make. That signature removes protection you may never notice is missing from your policy until you need it most.

Review your limits and endorsements at each renewal to confirm your coverage selections still match your actual financial situation.

Final takeaways

Getting uninsured motorist coverage explained clearly before an accident happens is one of the most practical steps you can take to protect your finances. Mississippi and the greater Memphis area see some of the highest rates of uninsured drivers in the country, which means the risk of facing this situation is real and not theoretical. UM and UIM coverage stand between you and significant financial loss when the at-fault driver cannot cover what they owe.

Review your current policy limits today, confirm you have not signed away UM coverage through a waiver, and consider raising your limits to match your actual income and medical cost exposure. If you have already been hurt in a crash with an uninsured or underinsured driver, acting quickly matters . An attorney can help you push your insurer to pay the full value your policy allows. Contact Mayfield Law Firm, P.A. for a free consultation about your accident claim.